What are the market conditions for woodworkers involved in the construction-based sectors and what are some of the investments being planned to improve their capabilities?

For perspective, the total value of private construction (residential and nonresidential) put in place in the United States was nearly $1.5 trillion ($1,435 billion) in 2022, up 12.1% from $1,279 billion in 2021. Spending increased in all residential categories in 2022, including a 4.4% increase for single family, a 4.4% increase for multi-family, and a 31.4% increase for residential improvements. Spending on nonresidential construction also increased by 9.8%. However, these increases in private construction spending amounts reflect, in part, inflationary prices throughout 2022.

The number of single-family housing units started in 2022 was 1,005,200, which marked a decrease of 10.8% from 2021. This decrease follows ten consecutive years of increases. Single family starts still are well below the peak of nearly 1,716,000 units in 2005, according to U.S. Census Bureau figures. In comparison, multi-family starts were 547,400 in 2022, up 15.5% from 2021 and the highest since this housing study series began in 2009.

Against this backdrop, the 14th annual housing market study was conducted in early 2023 to assess market conditions for secondary woodworking manufacturers involved in construction-based and related sectors. Information is provided on the status and current activities of manufacturers, as well as an analysis of what has changed since last year. This study is a joint effort by Virginia Tech, the USDA Forest Service, and Woodworking Network/FDMC (see “About the Survey” at the end of the article for details about the design of this year’s study).

Changes in sales & markets served

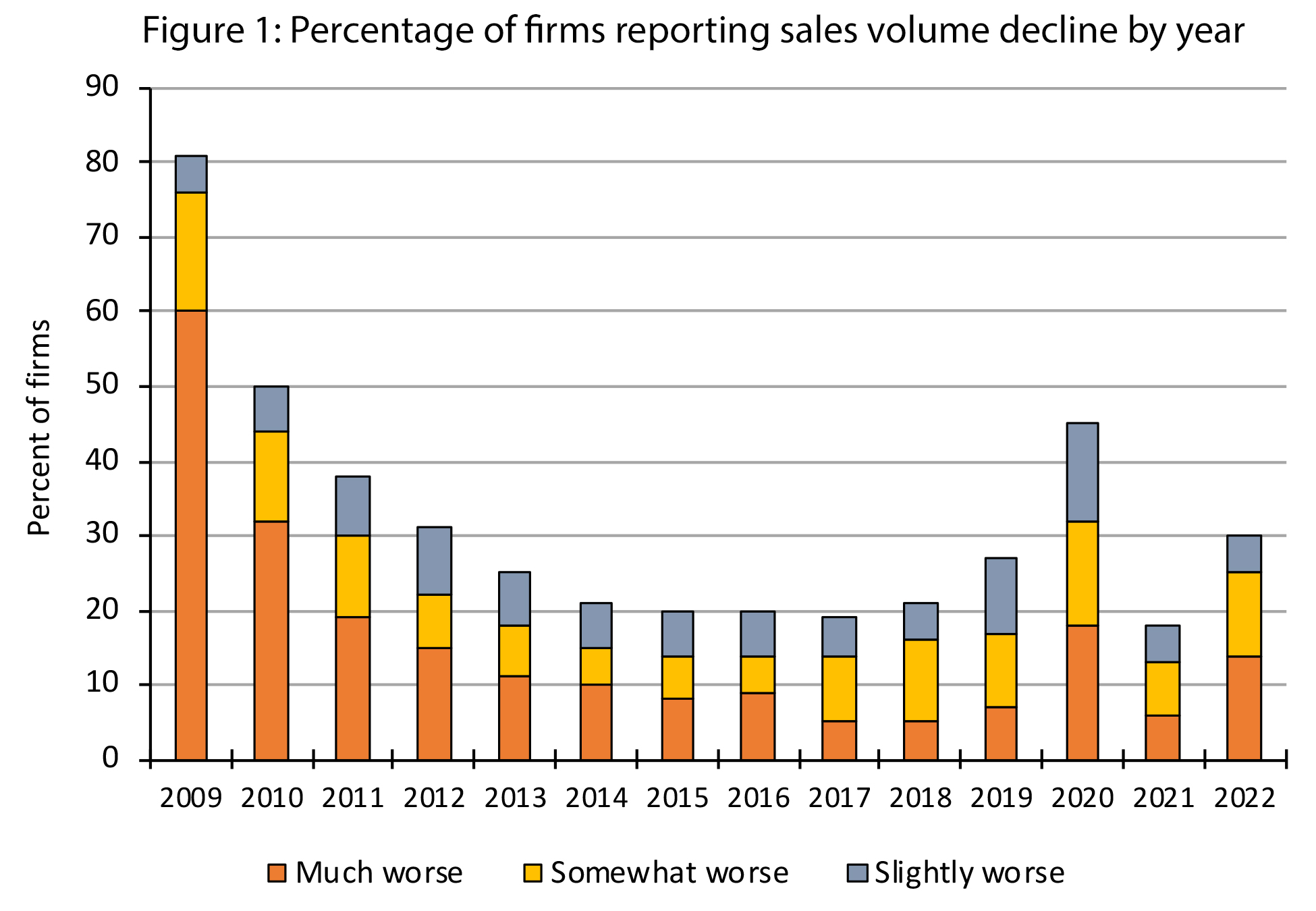

Analysis of year-over-year sales performance reveals a somewhat stable environment for secondary manufacturers until 2020, when the number of firms reporting a decline in sales volume spiked (45%) in connection with the COVID-19 pandemic. For 2021, the impacts of the pandemic seemed to abate with only 18% of firms reporting a sales volume decline, a percentage similar to pre-pandemic levels (Figure 1). However, for 2022, there was a notable increase in firms reporting sales volume declines (30%). Compared to 2021, the largest increase was in firms reporting sales were “Much worse” (+8 percentage points). The largest decrease was in firms reporting sales were “Much better” (-13 percentage points).

Why was sales volume down for many firms in 2022? Respondents largely attributed a downturn in the housing market and a decline in the overall economy (Figure 2). The housing market has not scored as such a prominent perceived factor in sales declines since 2012. Although scoring lower overall, it seemed respondents also noted an increase in both offshore competition and domestic competitors in 2022, perhaps reflecting that the relative strength in housing construction in 2021 attracted more business activity.

Even though 30% of respondents lost sales volume in 2022, another 55% of respondents reported sales volume increases while 15% reported no change in 2022 compared to 2021. The main factor attributed to success was simply growing in proportion with the overall economy.

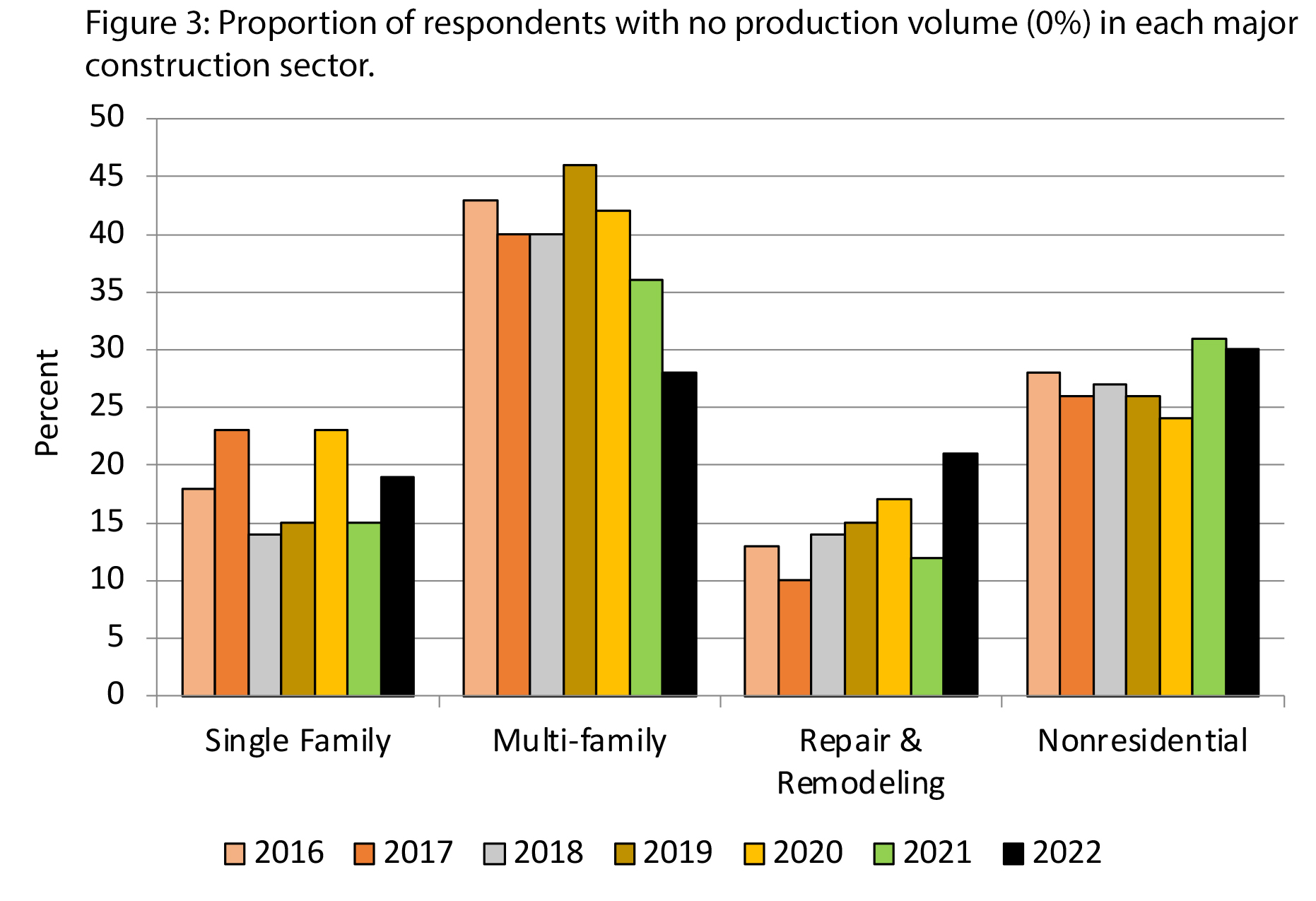

For 2022, 35% of respondents had most of their production volume (61-100%) associated with single family housing. This percentage was 13% for multi-family, 18% for repair and remodeling, and 9% for nonresidential construction. This shows the relative importance of single family housing construction to the secondary woodworking industry. However, as shown in Figure 3, firms have been shifting more activity to multi-family housing in recent years. Just 28% of respondents indicated that none of their production volume was associated with multi-family housing in 2022; this figure was 46% in 2019.

Green building products are another market possibility for secondary woodworkers to leverage sales volume. However, across most study years, the number of respondents indicating they have seen increased interest from customers seeking to source products compliant with green building standards programs has declined. This year, 27% of respondents reported they had seen an increase. Most respondents continued to indicate they had not seen an increase (52%), with the remaining 21% being uncertain if interest for green products had increased.

Demand for made-to-order (MTO) production continues to be important for the woodworking industry. However, MTO production has been declining in recent years of the study. For the past two years, less than half of the study respondents indicated that MTO production was greater than 4/5 of their product mix (49% and 47%, respectively). This figure was 70% of respondents in 2010, the first year of the study. Lastly, respondents to this year’s survey continued to be domestically focused, with 84% indicating that more than 60% of their sales in 2023 would result from domestically produced and/or sourced products. Conversely, 32% of respondents indicated that they had increased the use of wood imports in their respective product lines over the past five years. The industry also continues to target higher price points, with 56% of respondents reporting they operated at medium-high to high price points in 2023 compared to 54% in 2022.

Planned investment activities

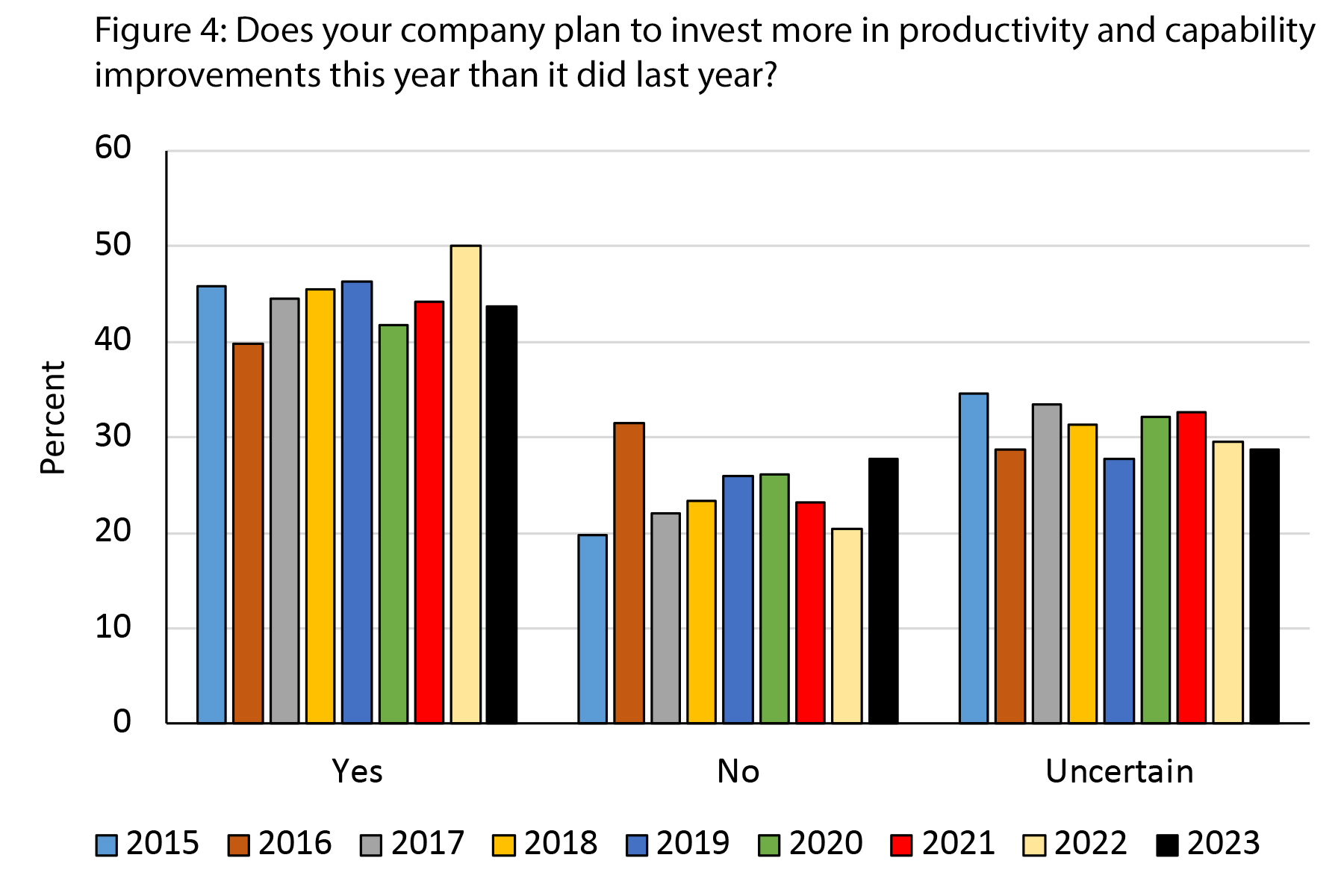

For 2023, 44% of respondents indicated that their respective firms planned to spend more than in 2022, which was similar to past years but down from the highest mark last year (Figure 4). Conversely, about 28% of respondents did not plan to spend more on business investments, which was an increase from last year. Lastly, 29% of respondents were uncertain of their firm’s investment plans, which was similar to previous years.

When asked about their firms’ investment plans over the next three years, 54% of respondents in this year’s study indicated they would spend less than $250 thousand, which was lower than most years but up slightly from last year. The percentages of respondents in the higher investment categories were similar to past years, with 28% indicating their firms would spend from $250 thousand to $1 million.

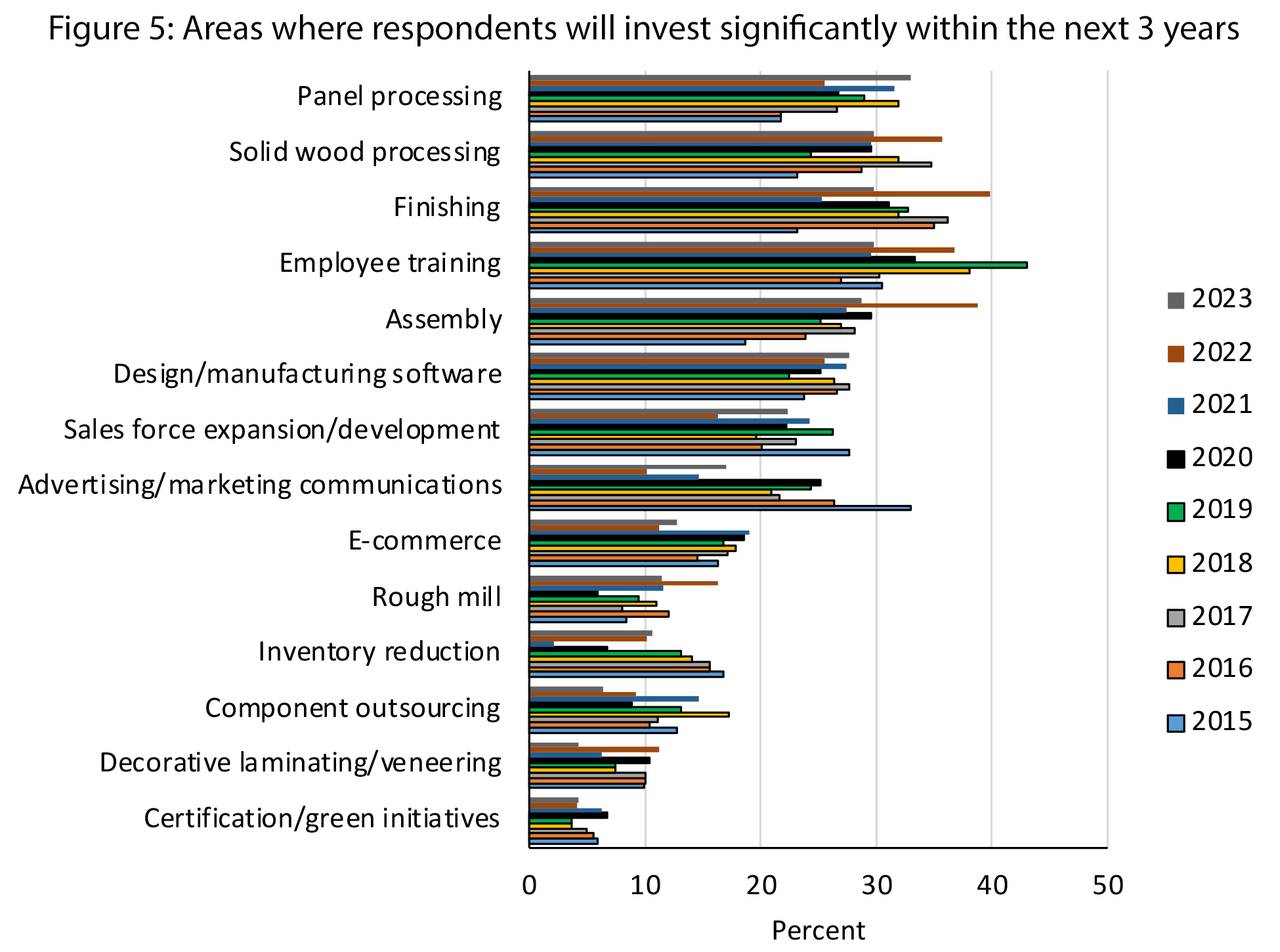

The study also assessed the general categories or areas where investments were planned over the next three years (Figure 5). Similar to recent years, several manufacturing-based investments continue to appear at the top of the list. For this year’s study, panel processing (33%), solid wood processing (30%), and finishing (30%) scored highest, followed closely by assembly (29%) and design/manufacturing software (28%). Employee training scored relatively high as well (30%), which also is consistent with past years. However, several manufacturing areas saw a decrease in planned investments from last year.

Advertising/marketing communications, once the highest-ranked investment area in 2015, reached its lowest level in 2022 but rebounded by 7 percentage points in 2023. A similar trend was seen with salesforce expansion/development. Taken together, this suggests that many companies are beginning to redouble efforts on marketing to generate sales.

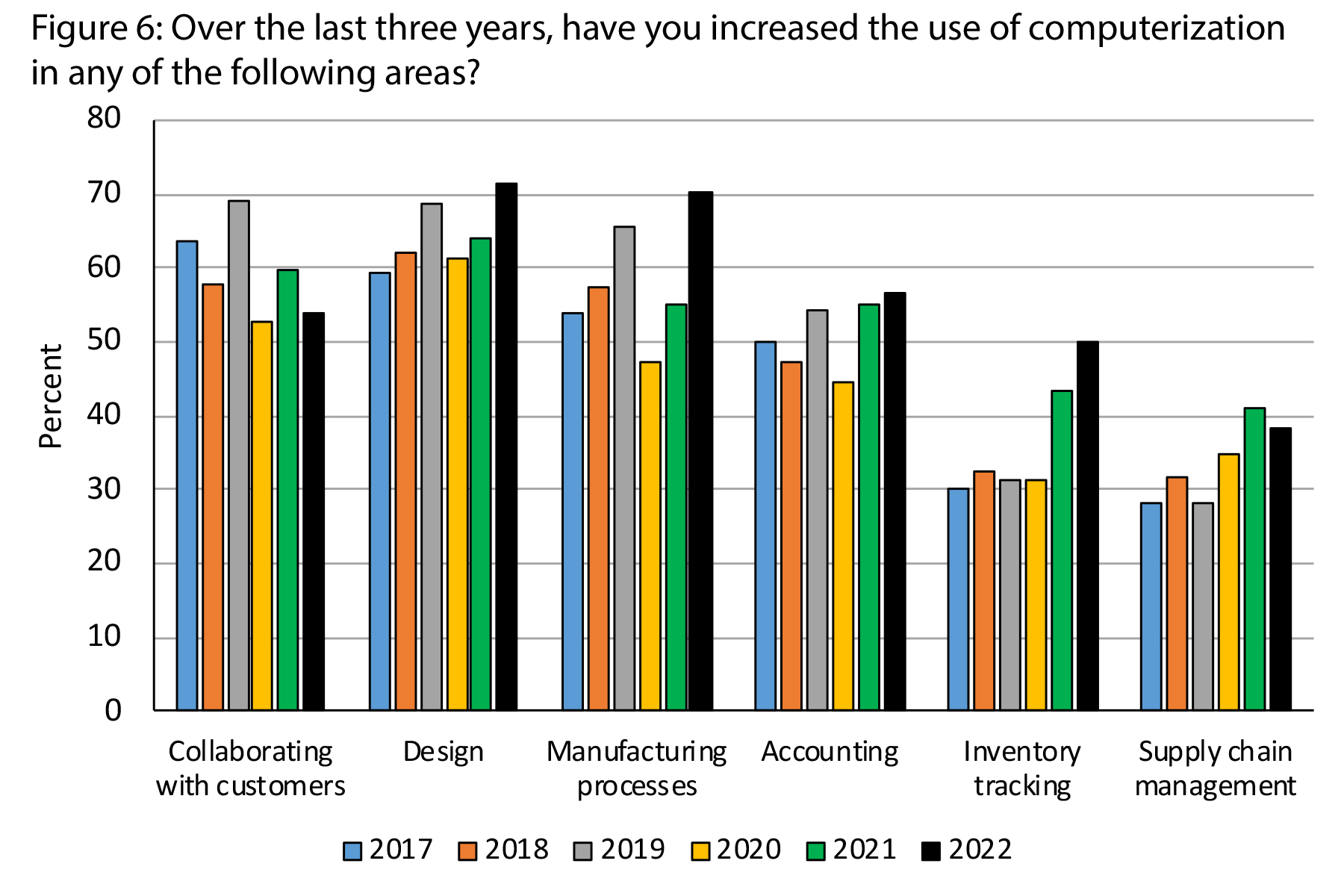

Lastly, respondents were asked to indicate if their firms had increased the use of computerization over the last three years in several functional areas. For the 2023 study, a majority of firms indicated they had increased computerization in design (71%), manufacturing processes (70%), accounting (56%), and collaborating with customers (54%). The largest recent growth has been with manufacturing processes and inventory tracking, which have increased by 23 and 19 percentage points, respectively, between 2020 and 2022. (Figure 6.)

Summary

There was a noticeable increase in the number of firms reporting sales volume declines for 2022 as construction markets slowed from their 2021 pace. A downturn in the housing market was rated by respondents as the biggest cause for sales declines, which corresponded with the first decline in single family housing starts in ten years. Plans for business investments cooled slightly from last year, but a plurality of firms (44%) still planned more investments for 2023 than they did in 2022. Panel processing, solid wood processing, and finishing led the list of areas where investments were planned over the next three years. However, in this year’s study, there also appeared to be movement to invest more in sales and marketing to generate new sales as construction markets slowed.

Recent study trends appear to show a desire to control costs as input prices and labor costs rise, illustrated in part by increased computerization in manufacturing processes and inventory tracking. There also has been a decline in made-to-order production, perhaps also an attempt to control costs by streamlining manufacturing. For example, “automation” and “lean” were mentioned by some firms when asked about actions they had taken to improves sales volume; interestingly these were mentioned by smaller firms (49 employees or less). At the same time, there seems to be a shift toward the multi-family housing sector even though the repair and remodeling sector has experienced the greatest growth in value since 2020. Still, single family housing remains the most important construction sector for respondents as a percentage of their overall sales volume.

About the survey

This is the 14th consecutive year for the Housing Market survey. While several of the questions remain the same from year to year to help track industry trends, more recent studies also have included questions related to investment and computerization activities. The 2023 study was conducted from February to April via e-mail invitations sent by Woodworking Network/FDMC to their subscribers. A total of 94 usable responses was received.

Similar to past years, kitchen/bath cabinet producers comprised the largest percentage of the sample, representing 41% of respondents. Fourteen percent of respondents were household furniture producers and another 14% were molding/millwork producers. Other types of producers in the sample included architectural fixtures (7%), dimension and components (6%), and office/hospitality/contract furniture (5%). While an additional 12% indicated their production was in “other” categories, many could reasonably be classified into one of the aforementioned categories; closets and craft accessories also were represented.

Most responding firms were relatively small, with 37% having sales of less than $1 million in 2022, and another 43% having sales of $1-$10 million. However, this was the first time in the study series that there were more respondents in the $1-$10 million sales category than in the < $1 million sales category, perhaps reflecting inflation in product prices. Furthermore, 62% of respondents had 1-19 employees and another 17% had 20-49 employees, which was similar to past years.

A majority of respondents (70%) held positions in corporate or operating management or were the owners of their respective firms. Responses were received from 35 states and provinces, with AB, CA, IN, MI, MN, MO, NY, OH, PA, and WI each accounting for at least 4% of the total responses. Geographic markets served ranged from a high of 50% doing regular business in the Midwest to a low of 20% doing regular business in the Southwest. Business conducted by respondents in all other U.S. regions (eight total) fell within this range.

About the authors: Matt Bumgardner is with the Northern Research Station, USDA Forest Service in Delaware, Ohio. Urs Buehlmann is with the Department of Sustainable Biomaterials at Virginia Tech, Blacksburg, Virginia. Karen Koenig is senior editor at FDMC/Woodworking Network.

Have something to say? Share your thoughts with us in the comments below.