Although material and labor shortages have construction and design firms reporting backlogs going into the fourth quarter of 2021, the industry overall looks to be rebounding for both residential and commercial projects.

The fourth quarter starts on a high note as architecture firms saw strong business conditions, according to the American Institute of Architects. October’s ABI score was at 54.3, with all sectors showing growth: Commercial/Industrial was strongest at 57.4, followed by Residential at 55.8 and Institutional at 51.4. Architecture firms are also projecting strong growth for 2022.

Meanwhile, architectural woodworkers continue to be cautiously optimistic heading into 2022, particularly as material costs continue to rise. Results of the AWI Cost of Doing Business Survey show continued decline of profitability and sales – “but overall, it’s not too bad.” While the average operating margin declined for the group as a whole, high-profit firms actually showed a slight increase. The Architectural Woodwork Institute also noted business sentiment is stronger across the board.

Custom manufacturers, including cabinetmakers, are also optimistic as they continue to benefit from increased remodeling during the pandemic. Conducted by the Cabinet Makers Association and FDMC/Woodworking Network, a recent survey of small and mid-size cabinetmakers found 2020 sales for the majority were the same or better than in 2019, with 2021 projected to be much better.

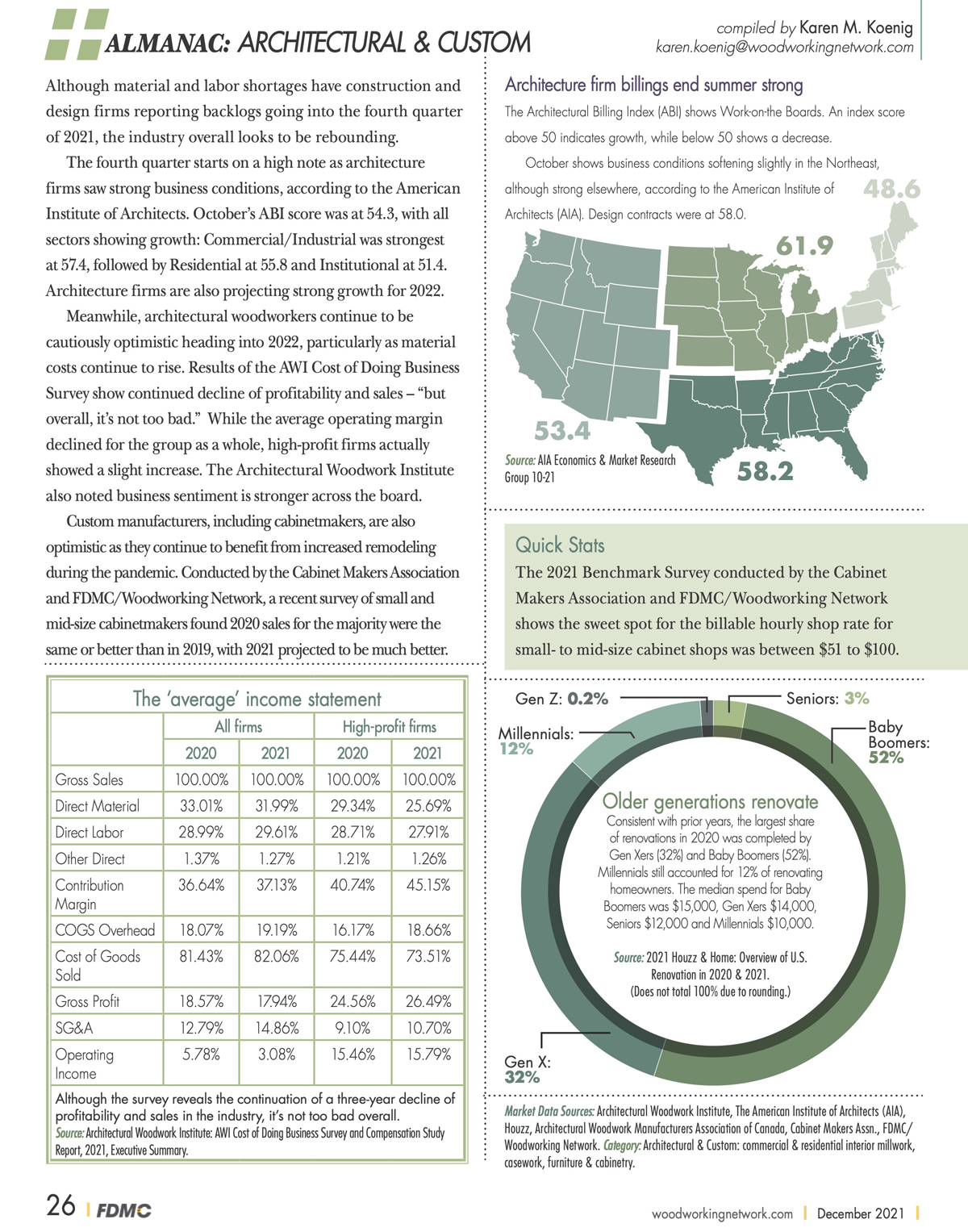

Architecture firm billings end summer strong

The Architectural Billing Index (ABI) shows Work-on-the Boards. An index score above 50 indicates growth, while below 50 shows a decrease. October shows business conditions softening slightly in the Northeast, although strong elsewhere, according to the American Institute of Architects (AIA). Design contracts were at 58.0.

See the infographic below. Find more market data in the December 2021 FDMC Wood Industry Almanac.

Quick Stats

• The 2021 Benchmark Survey conducted by the Cabinet Makers Association and FDMC/Woodworking Network shows the sweet spot for the billable hourly shop rate for small- to mid-size cabinet shops was between $51 to $100.

• Home renovation spending has grown 15% in the last year, to a median of $15,000, according to the 2021 Houzz & Home study. Higher-budget projects (with the top 10% of project spend) saw an increase from $85,000 or more in 2020, compared with $80,000 in the two years prior. The study provides an overview of U.S. renovation in 2020 and 2021.

• The new edition of the North American Architectural Woodwork Standards, NAAWS 4.0, became effective Sept. 1. Developed jointly by AWMAC and the Woodwork Institute, it includes a unified installation guide, expanded material uses, additional assembly methods and casework integrity testing.

• The trend toward hiring multiple pros for renovations continues, according to the 2021 Houzz & Home: Overview of U.S. Renovation in 2020 & 2021 study. Nearly 7 in 8 homeowners hired professional help during their renovations in 2020, consistent with previous years. They continue to hire more than one professional per project including specialty service providers (49%), construction professionals (36%) and professionals with design services (18%).

Market Data Sources: Architectural Woodwork Institute (AWI), The American Institute of Architects (AIA), Architectural Woodwork Manufacturers Association of Canada (AWMAC), Cabinet Makers Assn. (CMA), FDMC magazine, Houzz, LIRA/Joint Center for Housing Studies of Harvard University.

Category: Architectural & Custom: commercial & residential interior millwork, casework, furniture & cabinetry.

Find more market data in the December 2021 FDMC Wood Industry Almanac.

Have something to say? Share your thoughts with us in the comments below.