What are the market conditions for woodworkers involved in the construction-based sectors and what are some of the investments being planned to improve their capabilities?

For perspective, the total value of private construction (residential and nonresidential) put in place in the United States was more than $1.5 trillion dollars in 2023 ($1,541,063 million), up 4.7% from 2022 based on U.S. Census Bureau figures. This increase was driven largely by increased spending on nonresidential construction.

Spending decreased for single-family housing (-13.5%) and residential improvements (-4.6%) in 2023, even though spending on the smaller multi-family housing sector increased by 20%. Spending increased by 22.4% for nonresidential construction in 2023, following another relatively substantial increase (11.7%) in 2022.

The number of single-family housing units started in 2023 was 947,700, a 5.7% decline from 2022, which marked a second consecutive annual decrease after 10 years of increases. Single-family starts still are well below the peak of nearly 1,716,000 units in 2005. Multi-family starts were 472,200 in 2023, down 13.7% from 2022 even though overall spending on multi-family housing increased.

Against this backdrop, this 15th annual housing market study was conducted in early 2024 to assess market conditions for secondary woodworking manufacturers involved in construction-based and related sectors. Information is provided on the status and current activities of manufacturers, as well as analysis of what has changed since last year.

This study is a joint effort by Virginia Tech, the USDA Forest Service, and Woodworking Network/FDMC. (See “About the Survey,” below, for details about the study design and respondent characteristics.)

Changes in sales & markets served

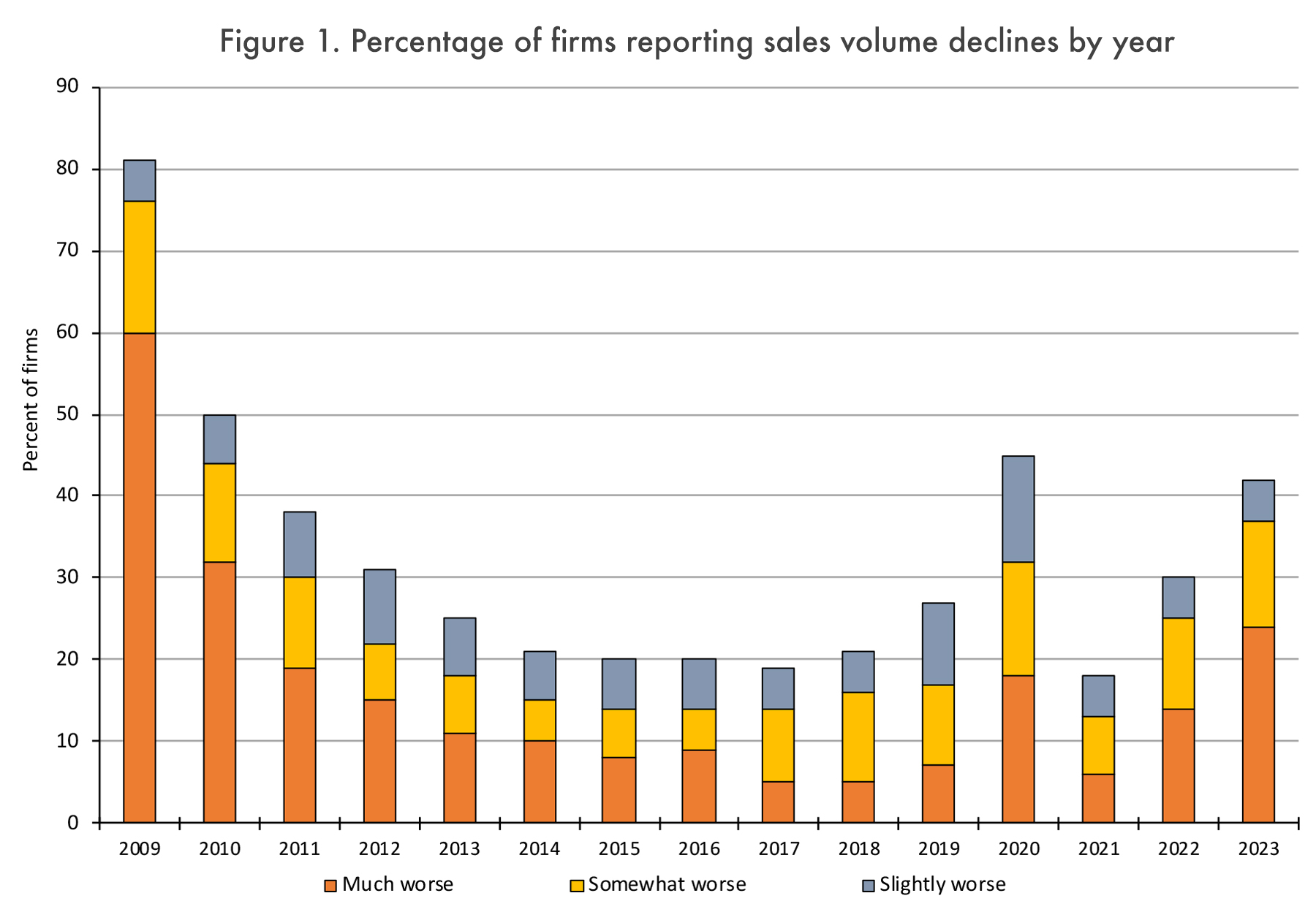

Analysis of year-over-year sales performance by study participants reveals a somewhat stable environment for secondary manufacturers until 2020, when the number of firms reporting a decline in sales volume spiked (45% reported that sales volume was “much worse,” “somewhat worse,” or “slightly worse”) in connection with the COVID-19 pandemic (Figure 1). For 2021, impacts of the pandemic seemed to abate, with only 18% of firms reporting a sales volume decline, a percentage similar to pre-pandemic levels. However, starting in 2022, there was a notable increase in firms reporting sales volume declines (30%), which continued in 2023 when 42% reported declining sales volume. The largest increase was in firms reporting that sales were “much worse,” which increased from 14% in 2022 to 24% in 2023.

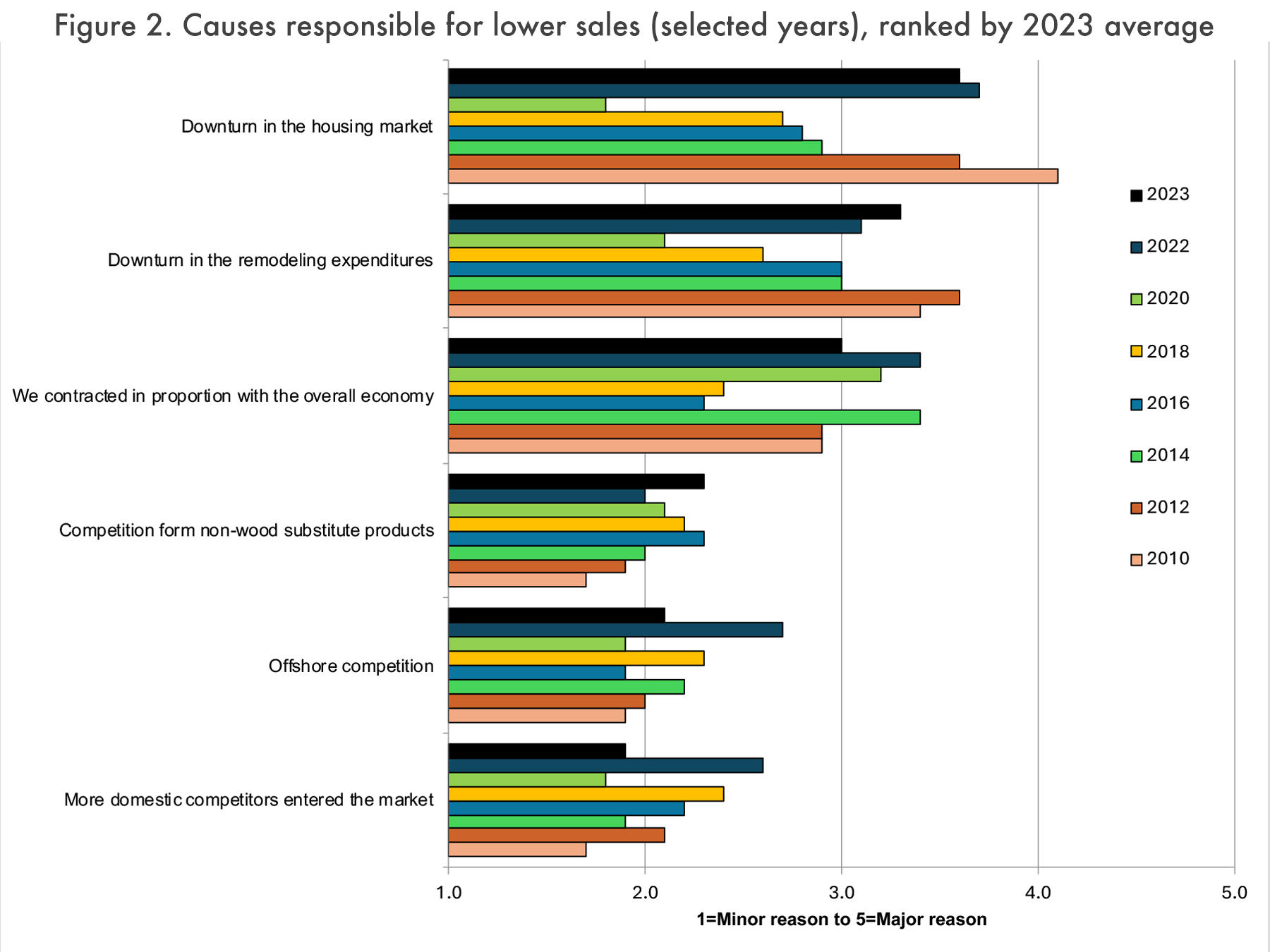

Respondents largely attributed their loss of sales volume in 2023 to a downturn in the housing and remodeling markets, followed closely by economic perceptions (Figure 2). As in previous years, offshore competition and domestic competitors scored relatively low as reasons for sales declines. Competition from non-wood substitutes also scored relatively low, but this category has had a minor general uptick since 2010.

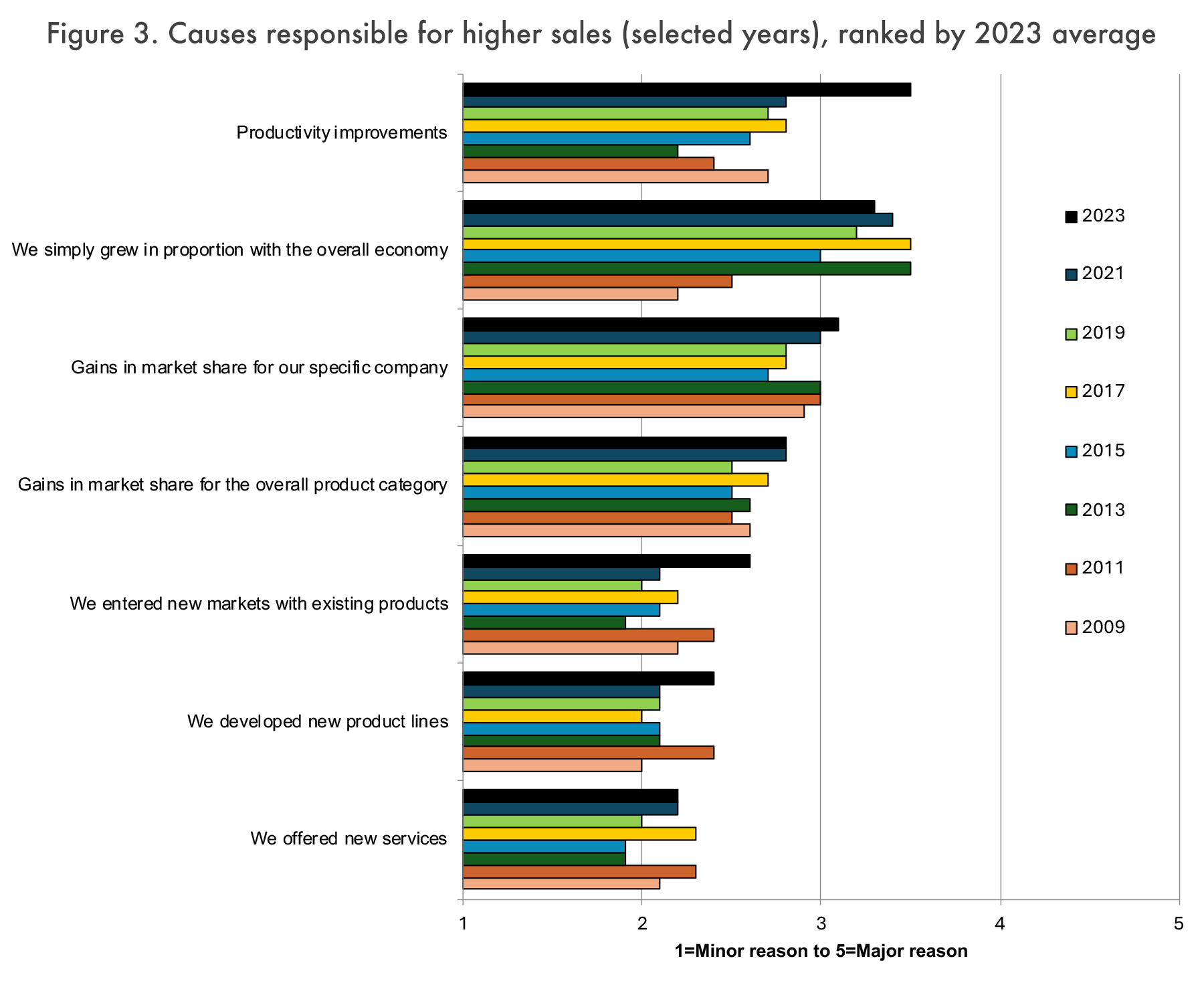

Even though 42% of respondents lost sales volume, another 45% reported sales volume increases while 13% were unchanged. These respondents attributed their success primarily to productivity improvements, which scored the highest in 2023 (Figure 3). This could mean that firms were able to increase output and sell the increased output, or that technology was being used to offset tight labor markets.

Growing in proportion with the overall economy also was rated somewhat highly. As a perceived reason for sales volume increases, the overall economy has consistently scored higher than individual firms’ activities, such as developing new products or new services.

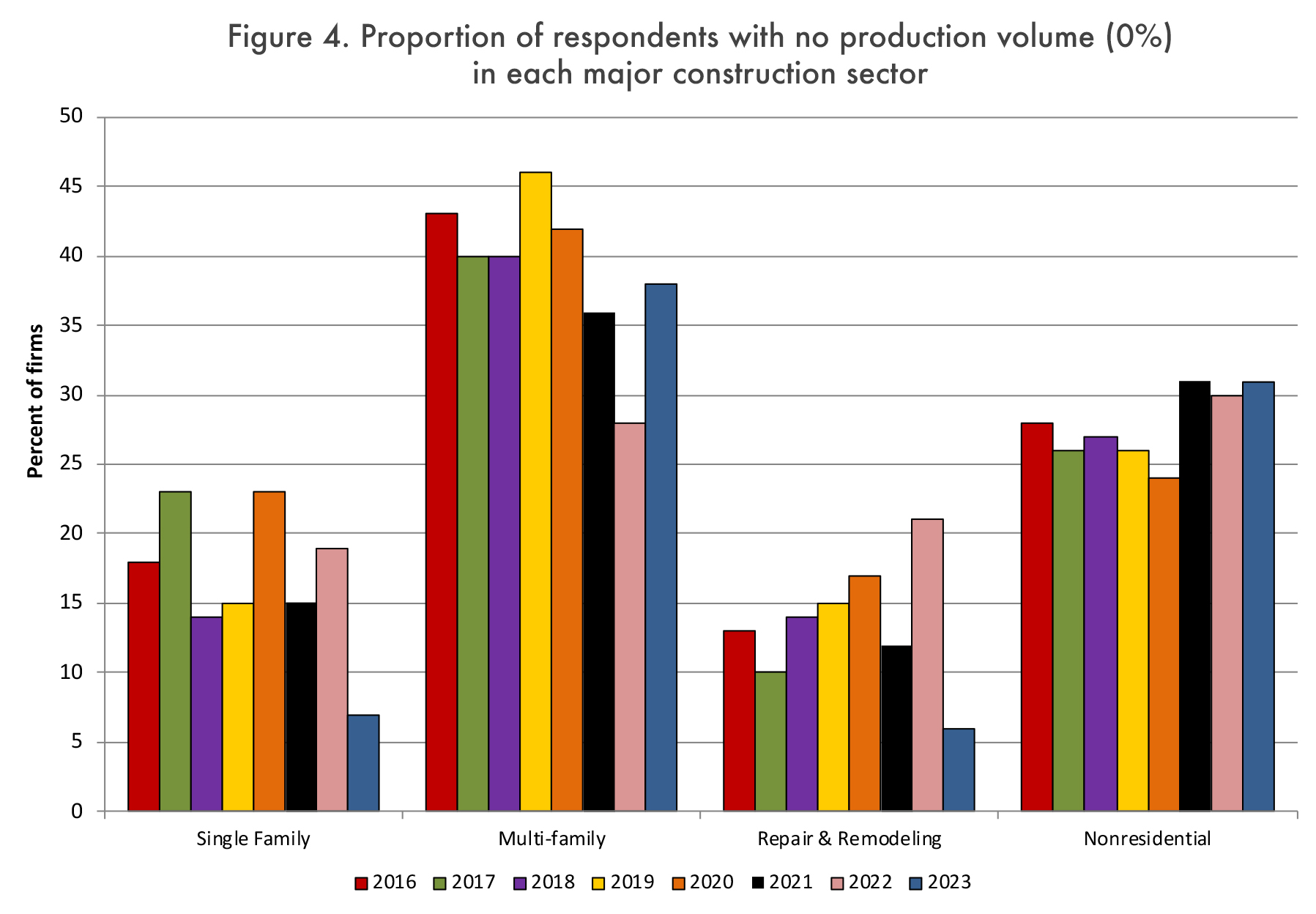

When asked where most (61%-100%) of their production volume was associated, 37% of respondents cited single-family, followed by remodeling (30%), nonresidential (10%), and multi-family (7%). This underlines the relative importance of single-family housing construction and repair and remodeling to the secondary woodworking industry. And, as shown in Figure 4, just 7% and 6% of respondents had no business activity in the single-family housing and the repair and remodeling markets, respectively, in 2023. This likely explains in part the decline in sales volume for many firms in 2023 given the softness in these markets.

Green building products are another market possibility to leverage sales volume. However, the number of respondents indicating they have seen increased interest from customers seeking to source products compliant with green building standards programs has declined, with just 28% of respondents reporting an increase in 2023.

Demand for made-to-order (MTO) production continues to be important for the woodworking industry. For 2024, 60% of respondents indicated that MTO production was greater than four-fifths of their overall product mix, compared to 49% and 47%, respectively, in 2022 and 2023.

Respondents were domestically focused, with 87% indicating that more than 60% of their sales in 2024 would result from domestically produced and/or sourced products. Conversely, 35% indicated they increased the use of imports (either lumber/components, finished products, or both) in their respective product lines over the past five years. The industry also continues to target higher price points, with 54% of respondents reporting they operated at medium-high to high price points in 2024.

Planned investment activities

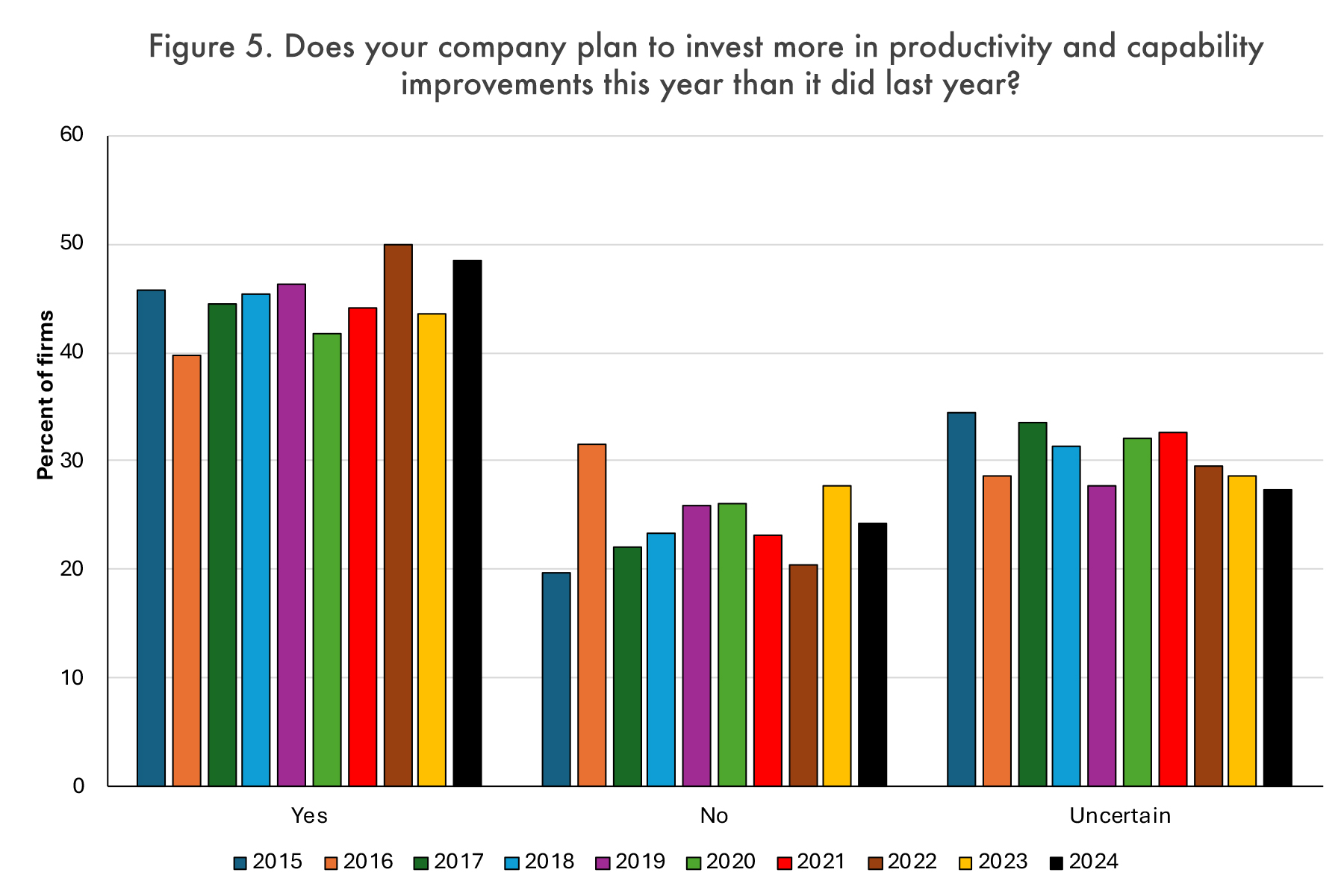

Similar to previous years, slightly less than half (49%) planned to spend more on investments in productivity and capability improvements in 2024 than in 2023, whereas 24% planned to spend less. Another 27% were uncertain (Figure 5).

When asked about their firms’ investment plans over the next three years, 54% of respondents indicated they would spend less than $250,000, which was about the same the past two years. The percentages of respondents in the higher investment categories were also similar to past years, with another 27% indicating their firms would spend from $250,000 to $1 million.

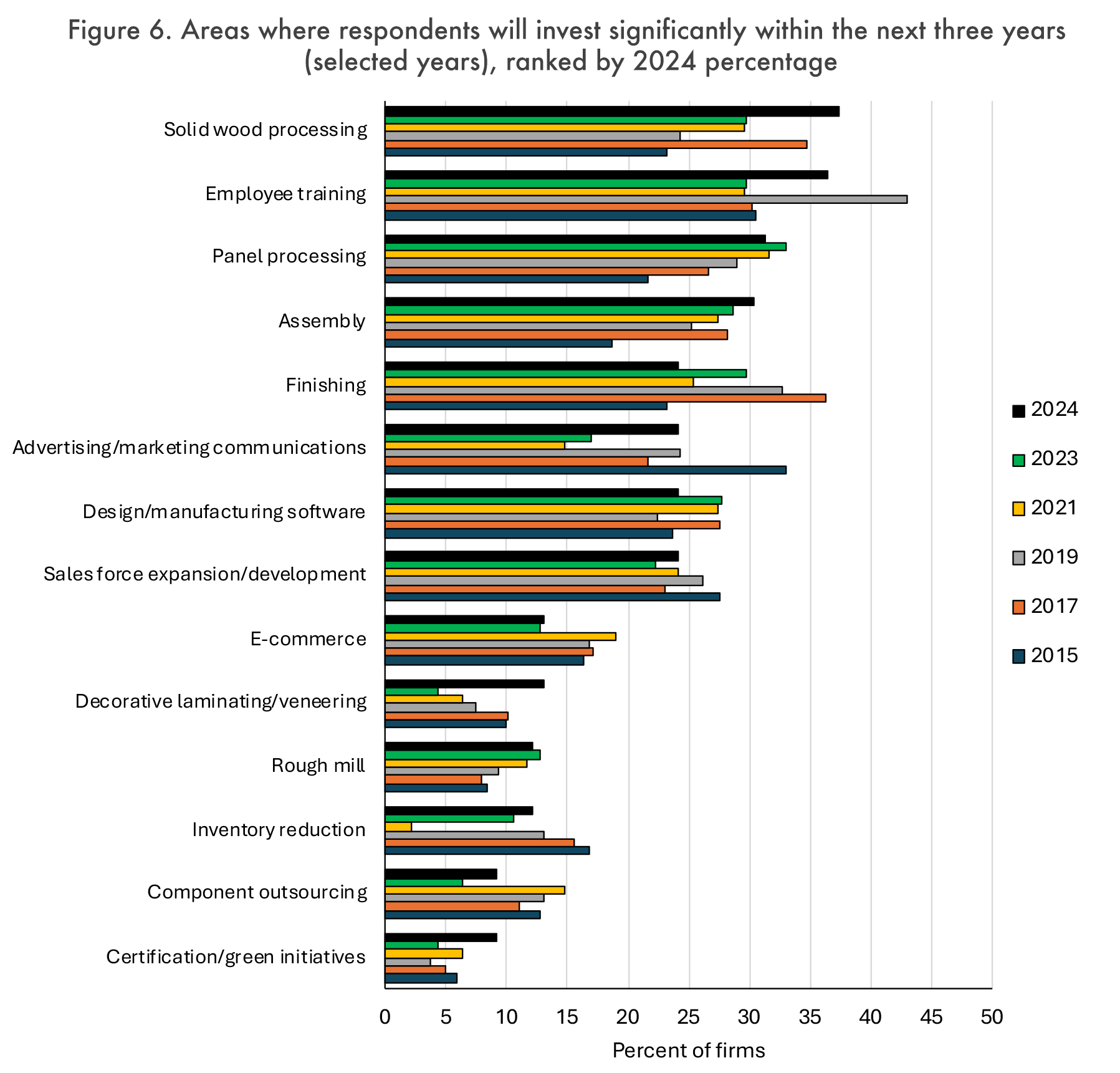

The study also assessed the general categories or areas where investments were planned over the next three years (Figure 6). As in recent years, several manufacturing-based investments remain at the top of the list. In addition, employee training continues to be a critical need for manufacturing firms. For this year’s study, solid wood processing (37%), employee training (36%), and panel processing (31%) scored highest, followed by assembly (30%).

The largest decline was for finishing which saw a 6% drop from last year, but with that said, finishing still was a relatively important investment area.

Advertising/marketing communications, once the highest-ranked investment area in 2015, hit its lowest level in 2022 but rebounded by 14 percentage points for 2024. This suggests that many companies are beginning to redouble efforts on marketing to generate sales to cope with slowing housing markets in 2022 and 2023.

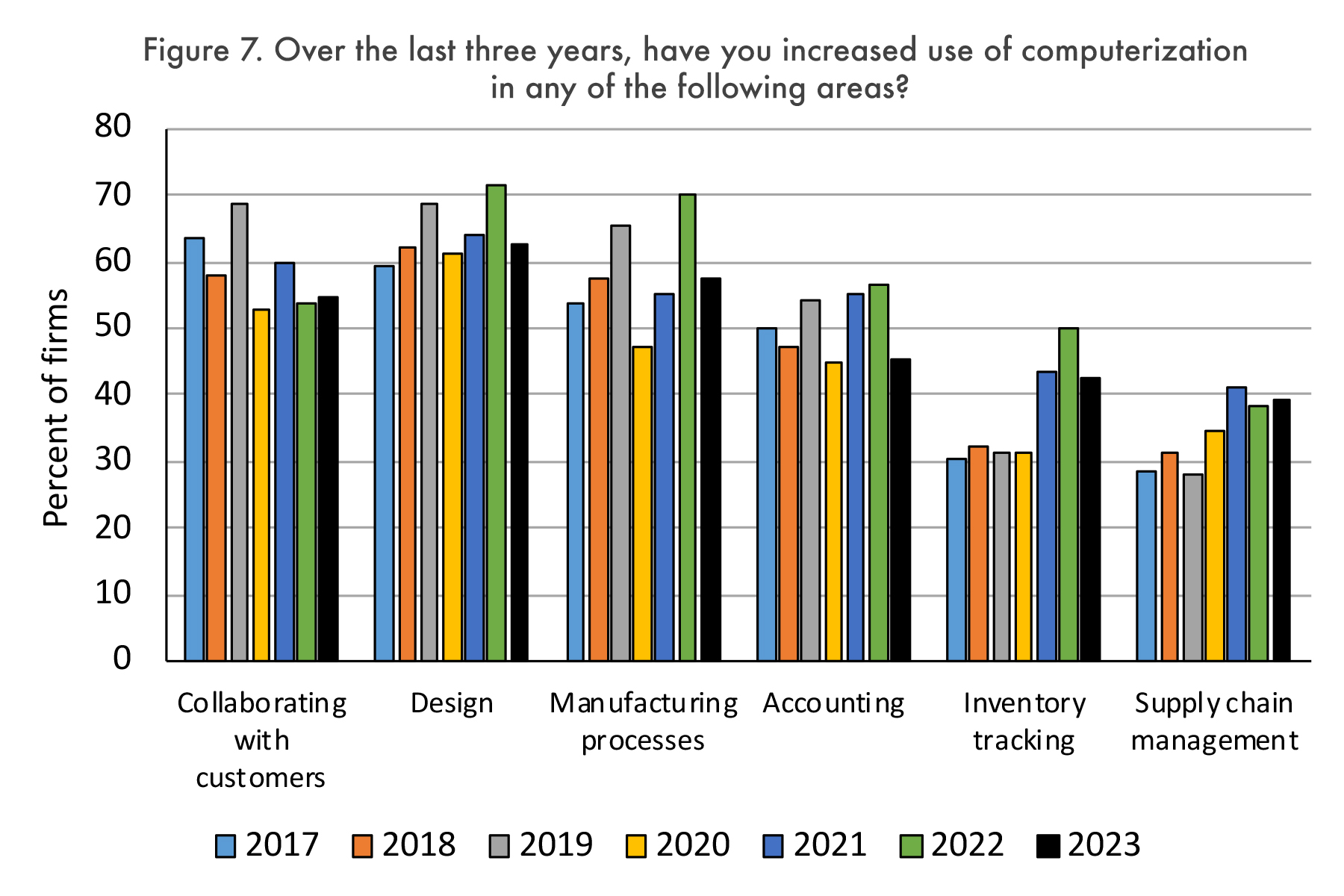

Respondents were asked to indicate if their firms had increased the use of computerization over the past three years in several functional areas. While most areas have shown an increasing trend since the question was first asked in 2017, most areas were slightly down in this year’s study (Figure 7). However, although relatively lower overall, inventory tracking and supply chain management seem to show an upward trend over the past few studies.

Summary

Notably more firms reported sales volume declines in 2023. According to respondents, this largely was a function of downturns in single-family construction and remodeling markets. Overall U.S. spending in these markets slowed in 2023 compared with 2022 even as respondents showed increased reliance on single-family housing and remodeling as part of their overall production volume relative to multi-family housing and nonresidential construction. Respondents indicated that they were investing in employee training at a relatively high level, and increasing productivity was viewed as the most important way to increase sales volume in the current market. Computerization in inventory tracking and supply chain management also were areas where there were upticks in investment.

Although most planned investment activities centered on manufacturing improvements, there also was a notable increase in advertising and marketing spending. This likely is a function of these firms trying to do more to generate sales as residential construction slowed — theory suggests that during downturns smaller firms tend to need to generate sales (marketing and advertising), whereas larger firms focus more on cost-cutting. Results also showed that investments in e-commerce remain relatively low despite exponential growth in the broader consumer economy. However, in the open-ended comments, some respondents did mention increasing efforts in e-commerce and internet marketing as actions they were undertaking.

About the survey

Now in its 15th year, the 2024 Housing Market survey was conducted from February to April via e-mail sent by Woodworking Network/FDMC to subscribers, receiving 99 usable responses.

As in past years, kitchen/bath cabinet producers comprised the largest percentage, representing 47% of respondents. Fourteen percent were household furniture producers, and another 12% were moulding/millwork producers. Other types of producers in the sample included dimension and components (8%), architectural fixtures (3%), and office/hospitality/contract furniture (3%). Although an additional 13% indicated their production was in “other” categories, most could reasonably be classified into one of the categories above; closets and home organization also were represented.

Most responding firms were relatively small, with 29% having sales of less than $1 million in 2023, and another 46% having sales of $1-$10 million. This was the second consecutive time there were more respondents in the $1-$10 million sales category than in the below $1 million sales category, perhaps reflecting continued inflation in product prices and/or improved productivity. Some 63% had 1-19 employees and another 13% had 20-49 employees, similar to past years.

Most respondents (67%) held positions in corporate or operating management or were the owners. Responses were received from 39 states and provinces, with CA, OH, NC, IN, TX, WA, FL, and WI each accounting for at least 4%. Geographic markets ranged from a high of 36% doing regular business in the Midwest to a low of 26% doing regular business in the Northwest.

About the authors: Urs Buehlmann is with the Department of Sustainable Biomaterials at Virginia Tech, Blacksburg, Virginia. Matt Bumgardner is with the Forest Products Laboratory, USDA Forest Service in Delaware, Ohio. Karen Koenig is senior editor at FDMC/Woodworking Network.

Have something to say? Share your thoughts with us in the comments below.