The home remodeling and organization industry is facing a 2026 market of sharp contradictions. While record-low homeowner mobility is creating a captive audience with significant pent-up demand, a severe affordability crisis and uncertain supply chains are putting pressure on project budgets and business operations.

Economist Chris Kuehl, managing director with Armada CI, in an October 2025 interview, highlighted this core conflict, noting a disconnect between hard data and public perception.

“You’re getting kind of a contradiction between how people are feeling and what the data is saying,” Kuehl said. “People are kind of doom and gloom... worried about inflation, they’re worried about unemployment.

“But then you start looking at the data, and it’s like, huh, we’re growing at about 3% which is faster than we normally grow,” Kuehl added. He pointed to “unemployment rates that are at record lows” and a high “quit rate,” which “is generally a signal that people are confident enough about finding a new job that they can just quit the one they have.”

Despite this statistical strength, annual spending on home improvements is projected to see growth soften to just 1.2% by the second quarter of 2026, according to the Leading Indicator of Remodeling Activity (LIRA) from the Joint Center for Housing Studies (JCHS) of Harvard University. This slowdown is tied directly to broader market weakness.

The ‘stay-put’ consumer

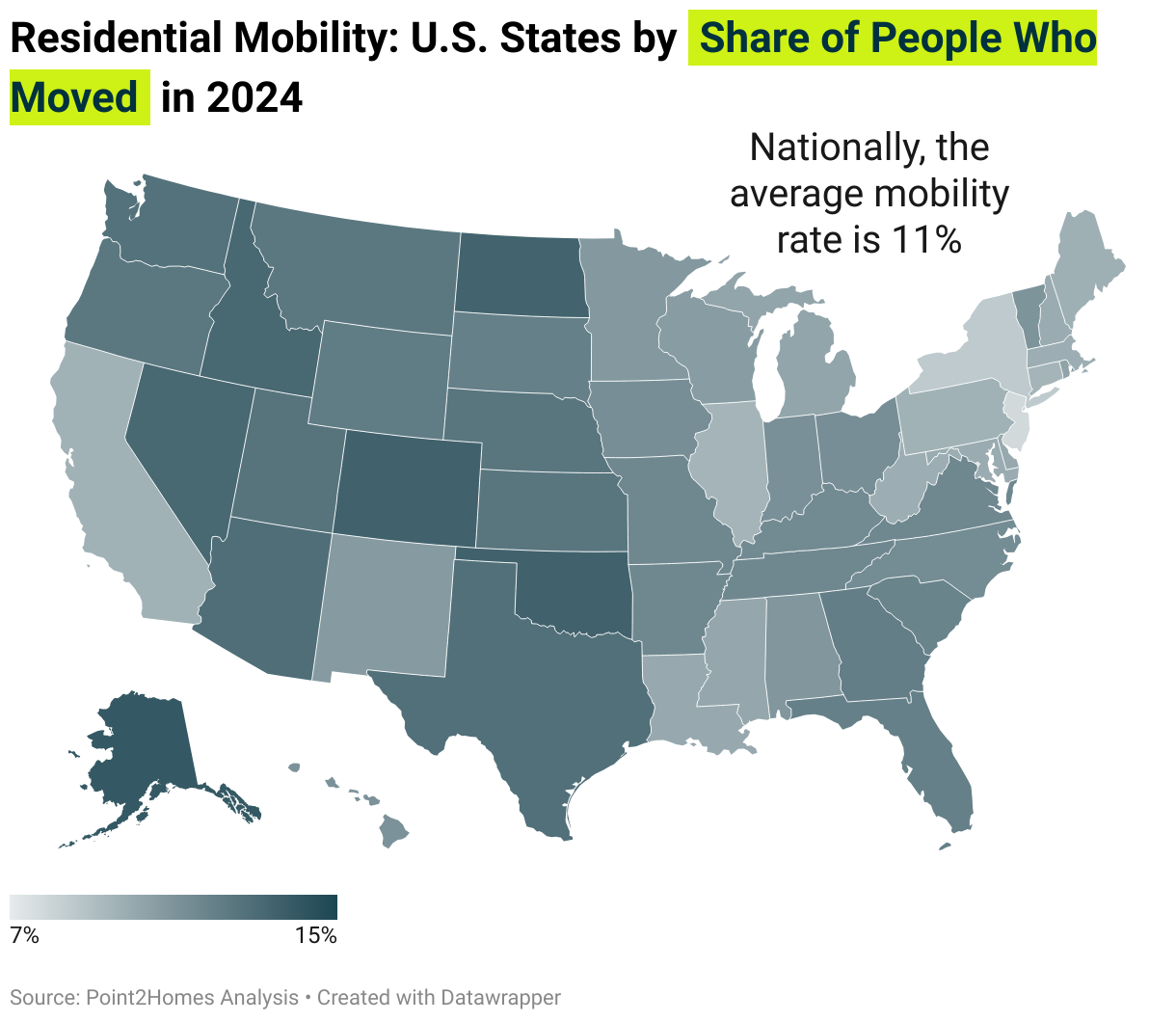

Compounding the contradiction is a countertrend: Americans are not moving.

The U.S. mobility rate hit its lowest point on record in 2024, with only 11% of Americans changing addresses, according to a Point2Homes analysis of U.S. Census data. This represents a stark decline from the 1960s, when nearly one in five Americans moved annually.

High home prices (although moderating a bit according to Kuehl), economic uncertainty, and elevated interest rates are the primary drivers forcing homeowners to stay put. This “lock-in” effect, combined with a housing market that saw existing home sales drop to a 30-year low, is compelling household owners to reinvest in their current properties.

For the home organization industry, this trend translates into opportunity. A 2025 U.S. Houzz Remodeling & Relationships Report found that after a project, 60% of couples felt “more comfortable” and 38% felt “more organized” in their home.

Affordability squeeze

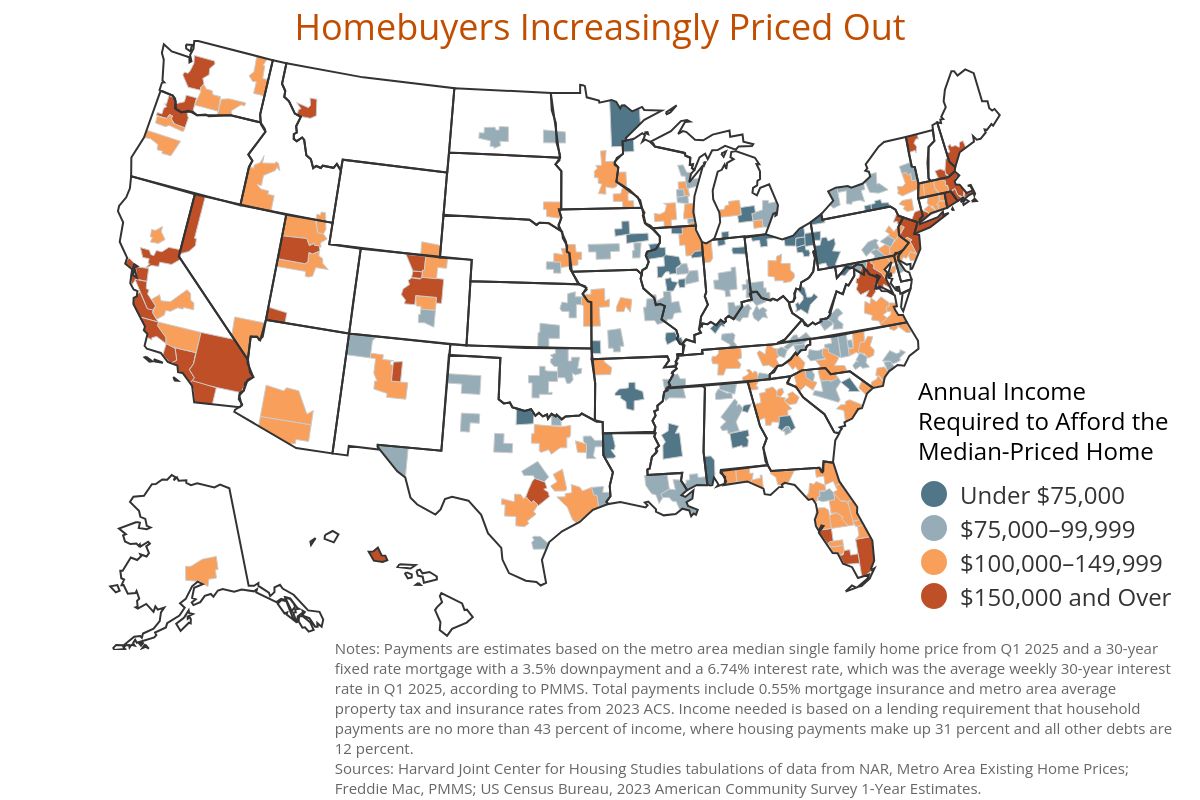

While homeowners are motivated to improve, their wallets are being squeezed. The 2025 State of the Nation’s Housing report from Harvard’s JCHS paints a sober picture of homeowner finances.

The number of cost-burdened homeowners rose to 20.3 million in 2023, driven by steep increases in insurance premiums (up 57% from 2019 to 2024) and property taxes.

Kuehl pointed out that this financial pressure is uneven, confusing the economic picture. “Oil prices have stayed down,” he said. “The price of homes has come down a bit. The price of cars has come down a bit. Meanwhile, food is going up. Things that are based on imports are going up. For obvious reasons. The tariffs are starting to bite.”

This pressure explains why “staying on budget” is the single biggest source of conflict for couples during a renovation, cited by 31% in the Houzz survey. Consequently, the top request from clients is “more transparent pricing and estimates,” according to 45% of couples.

The business operations nightmare

For businesses, delivering that transparent pricing has become nearly impossible. “The supply chain issue isn’t going away,” Kuehl warned. “If anything, it’ll probably get worse, because you’re kind of in the middle of a trade war, and your industry has a lot of product that comes from overseas.”

Kuehl identified an unstable and unpredictable trade and tariff environment as the primary culprit creating “paralysis” in the supply chain.

“Business is used to uncertainty... You never know what your competitor is going to do,” Kuehl explained. “But when it’s coming from government intervention, essentially, that becomes even more confusing, because there’s no rhyme or reason to it.”

This volatility has left businesses “very nervous about moving forward without really knowing what the rules are.”

“The biggest complaint I’m hearing from companies is, ‘I don’t care what the tariff is, just set one and don’t move it,’” Kuehl stated. “’But if it’s 20% today, 50% tomorrow, 10% on Thursday, 100% on Friday... what am I supposed to do with that?’”

This instability makes quoting jobs a gamble. “I can’t very well tell a customer it’s going to be between $30,000 and $190,000, somewhere in that range,” Kuehl said.

To combat this, many in the industry are adopting a high-risk inventory strategy: Overbuying materials to lock in current prices. “That saddles them with inventory costs,” Kuehl noted. This strategy is further complicated by shifting consumer moods and preferences. A business might stock up on a specific finish, only for trends to change: “Yeah, I know, but I watched HGTV, and they don’t do that anymore, so I don’t want it.”

Outlook for 2026

The new construction market offers little relief. While builders are finding some success with smaller homes, the median size declined for the third consecutive year in 2024, according to the JCHS. They are relying heavily on incentives. According to a September 2025 NAHB/Wells Fargo Housing Market Index report, 39% of builders reported cutting prices to boost sales, the highest percentage in the post-COVID period.

For the remodeling and organization industry, the 2026 outlook remains one of contradiction. The LIRA projection of a slowdown reflects a customer base constrained by the affordability crisis. However, the record-low mobility rate creates a captive audience that must adapt its current spaces.

Success in the coming year will hinge on a business’s ability to navigate extreme operational volatility while managing the budget-conscious demands of a “stay-put” consumer.

Are high-end closets insulated?

While Kuehl’s analysis paints a sober picture for businesses reliant on imports, Eric Marshall of the Closet Training Institute argues the high-end closet industry is uniquely insulated from this volatility.

The key difference, according to Marshall, is the supply chain. While kitchen cabinets are “either European or Asian imported into our country,” the closet industry is fundamentally different.

“There’s practically nobody that’s importing closet parts finished into the U.S.,” Marshall said in an October 2025 interview. “It’s [an]...American-made product. [Finished closet parts] are an American-made item.”

This domestic manufacturing base means the industry is not subject to the volatile 50% tariffs on European furniture and cabinets that have rocked other sectors.

Plus, the high-end closet business is shielded from the broader affordability crisis because it serves a different, wealthier clientele.

For this demographic, Marshall noted, the perception of the product has fundamentally changed. It is no longer a “someday” wish but a day-one essential. “She’s like, ‘I’m not moving [into] the house unless the closet is done,’ or ‘As soon as I get in the house, the first thing that’s happening is the closet.’”

Because the industry is somewhat insulated from tariffs and serves an affluent customer, Marshall argued that the smartest strategy for businesses in 2026 is to focus on and upgrade their core products.

Have something to say? Share your thoughts with us in the comments below.