British Columbia's secondary wood manufacturing firms showed low efficiency for most of the business types, and performance consistently lagged sawmill and panel sectors, with a “significant downward divergence” observed since the financial crisis, according to a study by Lili Sun, Rico Chan and Bryan Bogdanski of Natural Resources Canada’s Pacific Forestry Centre.

This low efficiency was mainly due to limited technical capability rather than to the scale of operations, according to the study published in the July 2026 issue of Forest Policy and Economics. For more analysis, see the complete study.

Some of the studies' revelations include:

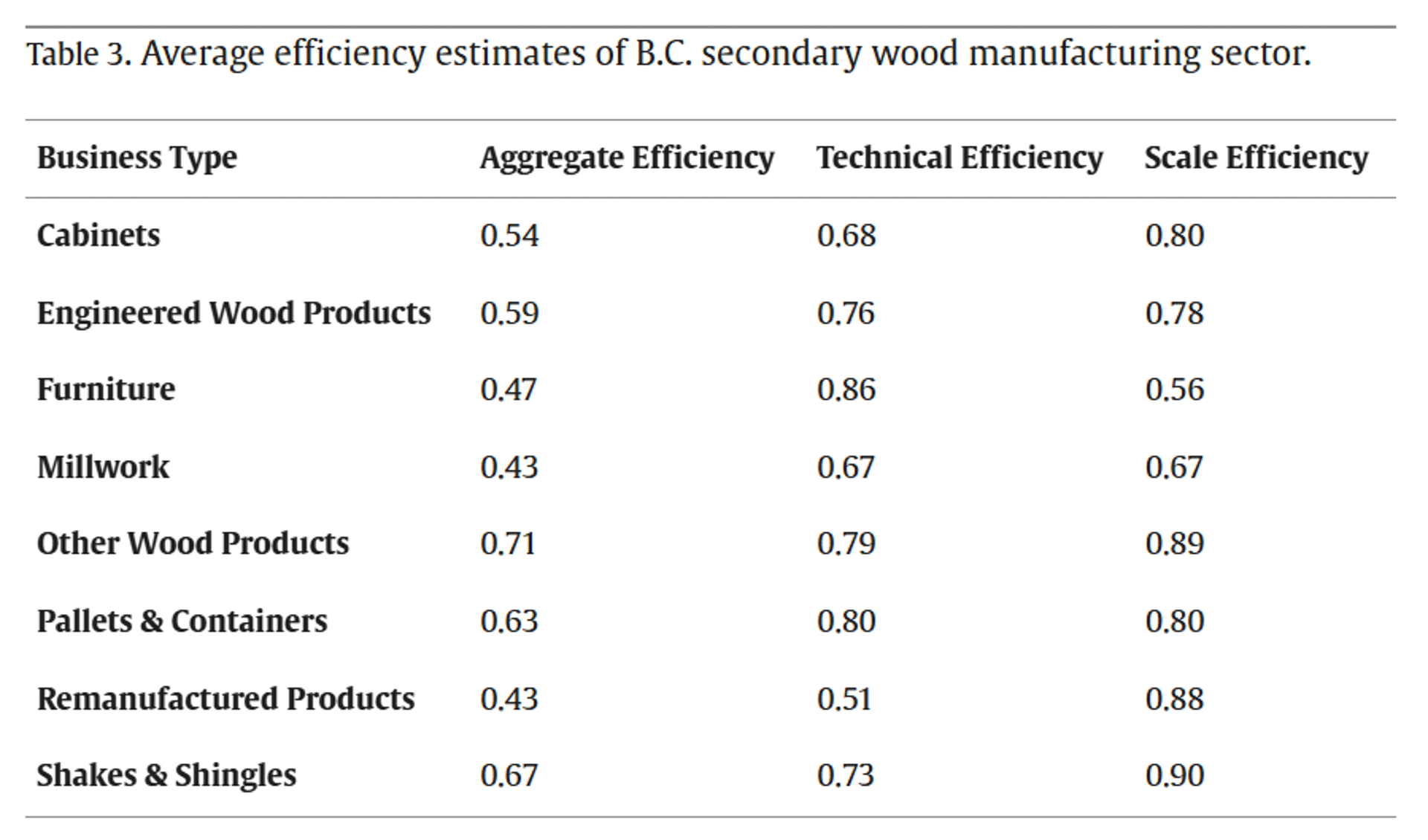

- While efficiency varied across business types, the sector's aggregate efficiency was generally low (0.43–0.71). The decomposition indicated that technical inefficiency dominated scale inefficiency for most business types; notable exceptions included Furniture, where scale inefficiency was more pronounced, and Millwork and Pallets & Containers, where technical and scale efficiencies were similar.

- The study states that the technical-efficiency scores imply firms could reduce input use by 14% to 49% without reducing output if they operated in line with best-practice firms within their business type. These efficiency scores were much lower in comparison to the sawmill sector scores calculated in a previous 2005 study. They found the average aggregate efficiency for BC sawmills was 0.8, and the scale efficiency and technical efficiency were 0.97 and 0.83, respectively. Investigation of the slacks variable values shows that 25% of firms could reduce one of the inputs to achieve additional efficiency.

- Only 17% of firms in the sample are fully efficient on the aggregate measure. The share varies by business type, with Other Wood Products at 55% and Cabinets at 7% on aggregate efficiency, and Millwork at 6%. The pattern differs on scale efficiency in some categories, including Remanufactured Products, where 17% of firms are scale-efficient but 70% are at or above 0.85 scale efficiency.

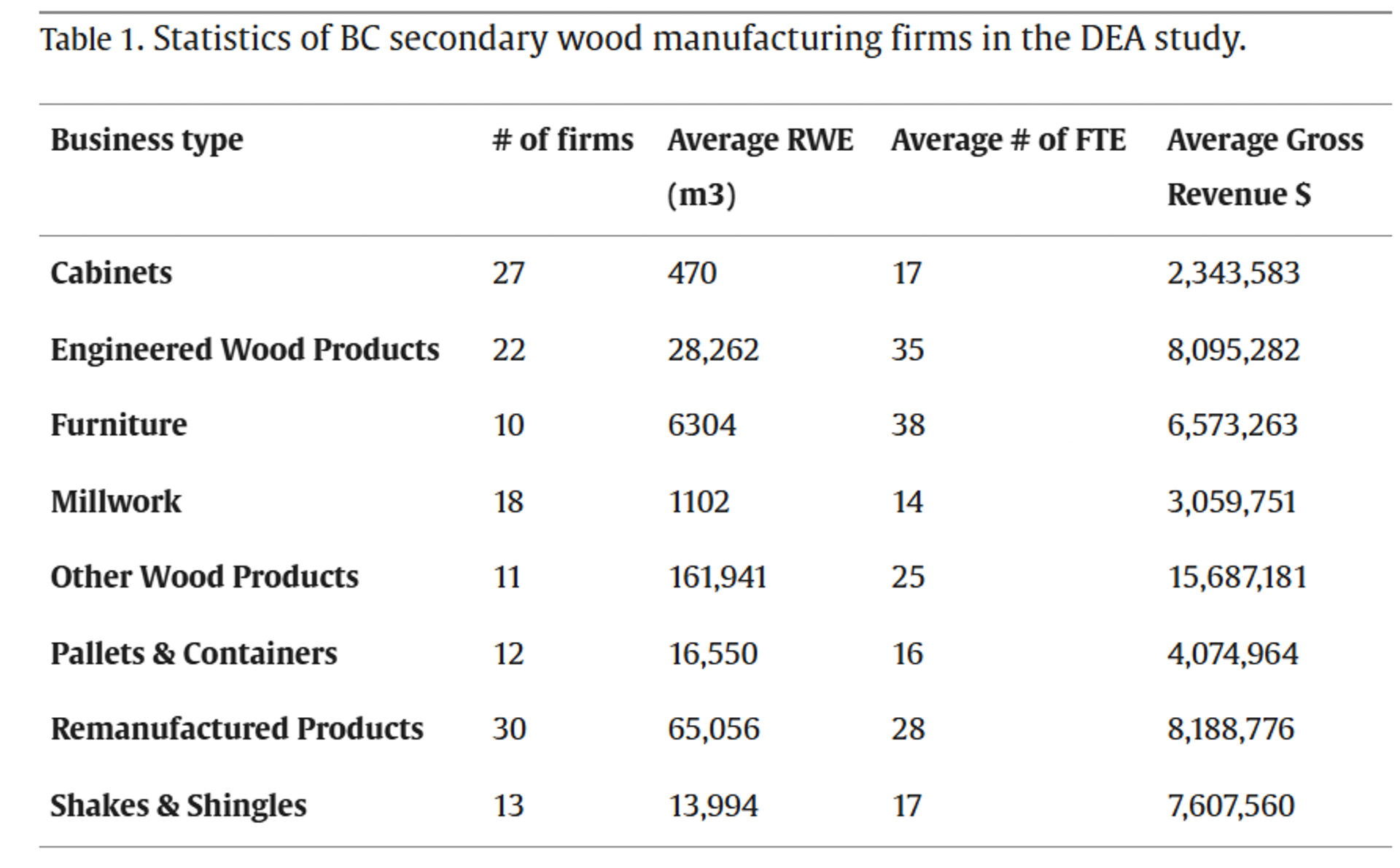

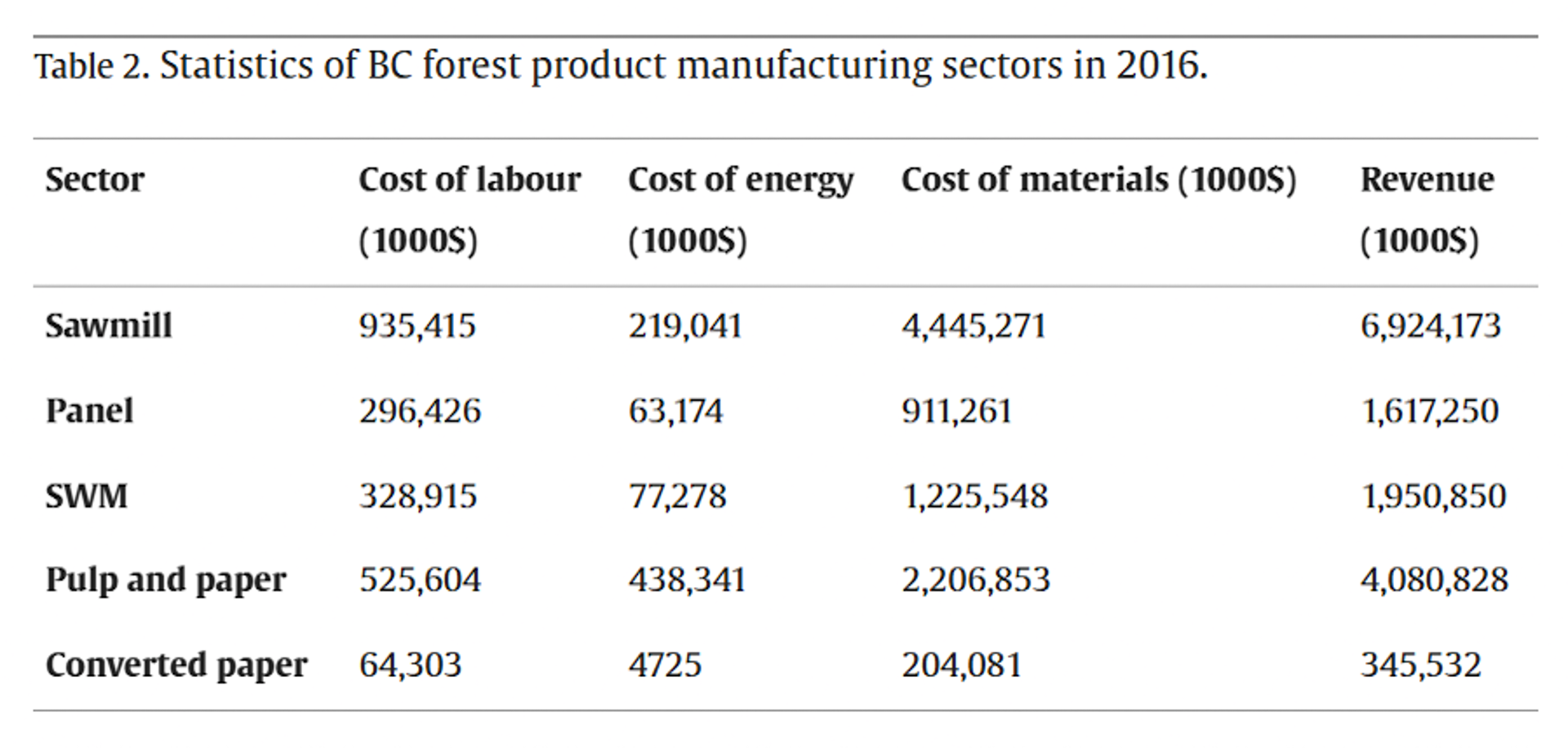

- The researchers studied the secondary wood manufacturing sector (SWM) using Data Envelopment Analysis (DEA), which is a mathematical modeling method used to measure the relative efficiency of similar business units, facilities, or processes, and Malmquist total factor productivity index (MPI), which is a data-driven economic tool used to measure changes in productivity over time, while incorporating data from both a survey on individual firms and sectoral data compiled by Statistics Canada.

- DEA results showed that BC's secondary wood manufacturing firms had low efficiency and the factor contributing to the inefficiency was a lack of technical capability as opposed to the scale of operations in most of the business types. The MPI results reveal that SWM consistently underperforms relative to the sawmill and panel sectors, with a clear divergence emerging after the 2007–2009 financial crisis.

- Weak productivity growth is largely attributable to limited and inconsistent technical change, reflecting a lack of innovation and adoption of new technologies. Policies aimed at supporting the sector could focus on factors improving firms' technical efficiency and frontier such as process optimization, technology adoption and innovation, and training and skill development.

- Productivity growth has been limited and uneven over the study period. While the early years show relatively strong gains, with MPI frequently exceeding unity, this momentum is not sustained, peaking at approximately 1.15–1.17 in the mid-to-late 1990s. The sector then enters a prolonged phase of stagnation and decline following the 2007–2009 financial crisis, during which MPI consistently falls below one and begins to diverge from upstream sectors, which show stronger recovery and sustained gains. Although a modest recovery emerges after 2016, with MPI hovering slightly above unity, the overall pattern points to weak long-run productivity performance in SWM. This divergence is pronounced during the COVID-19 period as well: while sawmill and panel industries experienced an exceptional rebound in 2021, SWM recorded modest growth.

Have something to say? Share your thoughts with us in the comments below.