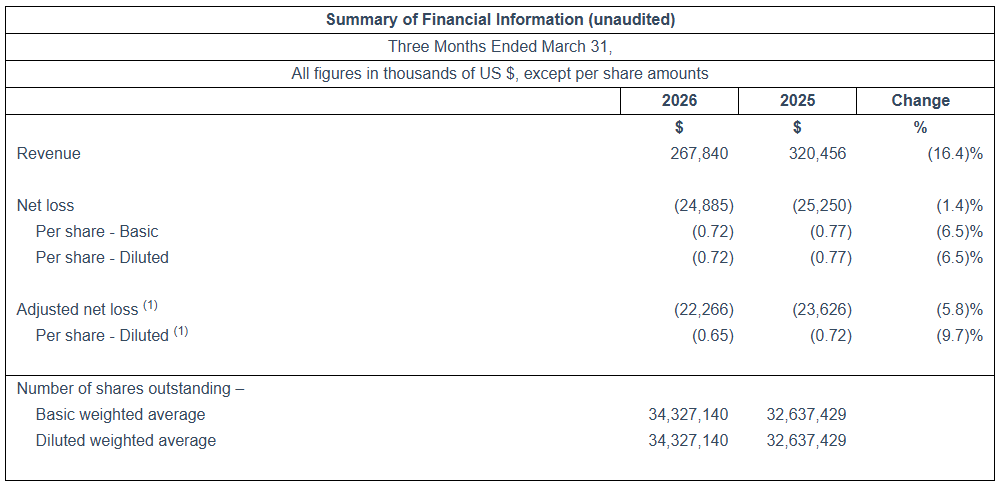

MONTRÉAL — Dorel Industries Inc. has announced its financial results for the first quarter ended March 31, 2026.

First quarter revenue was $267.8 million, down 16.4%, from $320.5 million a year ago. Reported net loss for the quarter was $24.9 million to $25.3 million a year ago. Adjusted net loss for the quarter was $22.3 million compared to $23.6 million a year ago.

“Dorel Juvenile delivered a solid first quarter, demonstrating resilience in a volatile global environment marked by geopolitical uncertainty, foreign exchange headwinds, and rising input costs. Strong growth and improving profitability across Europe and International markets, including Export, Australia, and Latin America, helped offset softness in the U.S. business. Disciplined cost management supported performance despite margin pressure from currency movements, while continued investment in innovation and strong global customer engagement reinforced the strength of Dorel Juvenile’s diversified portfolio and its positioning for sustainable growth.”

“Dorel Home results improved meaningfully compared to both prior year and last year’s fourth quarter, but this was due only to substantial reductions in overhead and operating expenses. Sales were disappointing due to a lack of success in certain traditional furniture categories. As evidenced by the recent announced closure of two competing Canadian-based furniture manufacturers, the furniture industry remains very difficult. This is forcing us to be even more focused on exiting categories and channels where our competitive advantage is limited and continue with a product line that minimizes our overhead structure. This will allow us to return to profitability and provide a clearer foundation for future success as the year progresses,” stated Dorel President & CEO, Martin Schwartz.

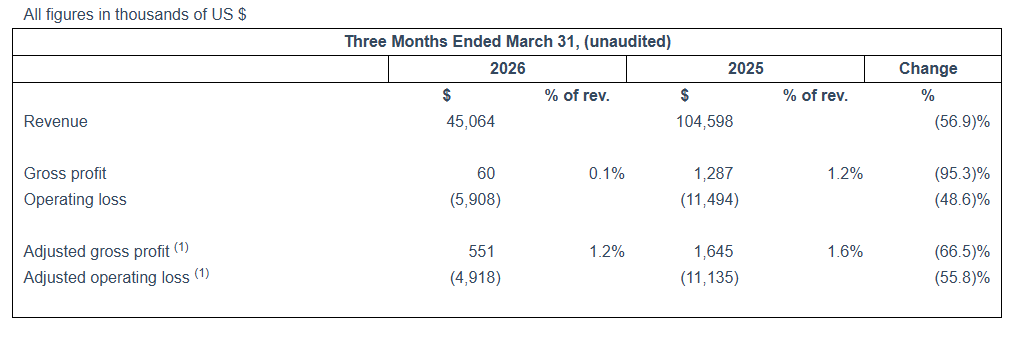

Dorel Home

Revenue for the first quarter was $45.1 million, a decrease of $59.5 million from $104.6 million last year. While revenue declines were anticipated given the new operating model of the Home segment, the overall sales level in the quarter was below expectation and was not sufficient to offset the reduced cost structure even though sales of Cosco branded products, the predominant business, performed near plan. As a result, the adjusted operating loss1 for the quarter was $4.9 million compared to $11.1 million in the prior year.

Inventory availability improved slightly in the quarter, but continued to hamper sales, particularly for items sold via the e-commerce channel of distribution. In addition, our ability to compete in certain product categories resulted in a significant sales shortfall in those categories. Conversely, the Cosco branded line of folding furniture and step ladders was much closer to expectations, with the shortfall in the other categories triggering a further review of product lines and channels. In Europe, the business ran closer to plan and is aggressively working on broadening their customer portfolio with leading omni-channel retailers.

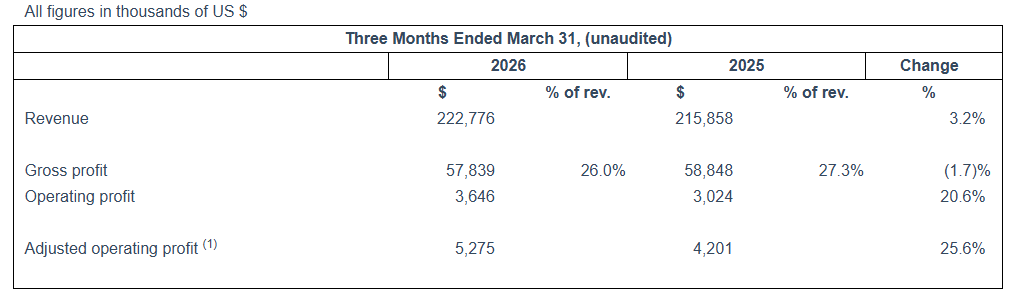

Dorel Juvenile

For the first quarter of 2026, revenue reached US$222.8 million, a 3.2% increase compared to the prior year. Adjusted for foreign exchange rate variations year-over-year, the organic revenue decline1 was 2.8% resulting from a decrease in sales in North America, partially offset by double-digit growth delivered across Europe and several international markets. Adjusted operating profit1 was US$5.3 million, an increase of US$1.1 million compared to last year. This was despite a decline in gross margins due principally to year-over-year variations in foreign exchange rates, which were more than offset by a reduction in operating costs.

In Europe and other international markets, improved results offset the challenges in the U.S. with both revenues and earnings increasing over prior year. Global sales of the flagship Maxi-Cosi brand increased almost 20% in the quarter and make up over 40% of segment sales. In the U.S., the revenue decline reflects continued softness in the juvenile category following tariff-related disruptions, heightened promotional pressure, and cautious consumer spending. Despite these challenges, operating expenses were significantly reduced year over year as management continued to align the cost structure to a lower-demand environment. While the U.S. market remains challenging, the Company continues to focus on targeted innovation, portfolio optimization, and selective customer programs to support longer-term recovery.

Innovation and customer partnerships remained key strategic priorities. In March, Dorel Juvenile hosted its annual Global Customer Conference in Algarve, Portugal, bringing together more than 240 customers from around the world. The event highlighted the Company’s parent-centric design philosophy and showcased major product innovations, including the launch of the new Maxi-Cosi Coral GO, as well as new collections and the proprietary SLIDETECH® 2 technology. Interactive product hubs encouraged hands-on engagement and real-time feedback, reinforcing strong customer confidence and generating positive commercial momentum, particularly within the nursery furniture portfolio.

Outlook

“Driven by our success outside the US. Market, the Juvenile segment performed well in the quarter. Looking forward, we expect the sales and earnings to improve in the U.S. and coupled with our on-going success in Europe and other markets, this gives us confidence that we will have a strong second half. Expectations are that adjusted earnings for full year 2026 will exceed prior year. While we are seeing some upward pressure on costs, we are actively engaged with strategic suppliers and addressing other costs to mitigate these headwinds,” commented Dorel President & CEO, Martin Schwartz.

“At Dorel Home, we are prudently re-assessing the business to identify our path forward. We intend to leverage our excellent retail partnerships in making choices on categories that make sense for them and improve our portfolio mix going forward. Cosco remains a leader in its product categories, and this has been particularly true as uncertainty around tariffs meant retailers were exploring alternate sources of supply and we are able to work with them from multiple jurisdictions. Fortunately, the work done last year in reducing our footprint to what is today, allows us to make any needed changes relatively quickly. While this is not likely to impact the second quarter, we expect that we can deliver profits in the Home segment in the medium to long term,” concluded Schwartz.

To view the full report, visit dorel.com.

Have something to say? Share your thoughts with us in the comments below.