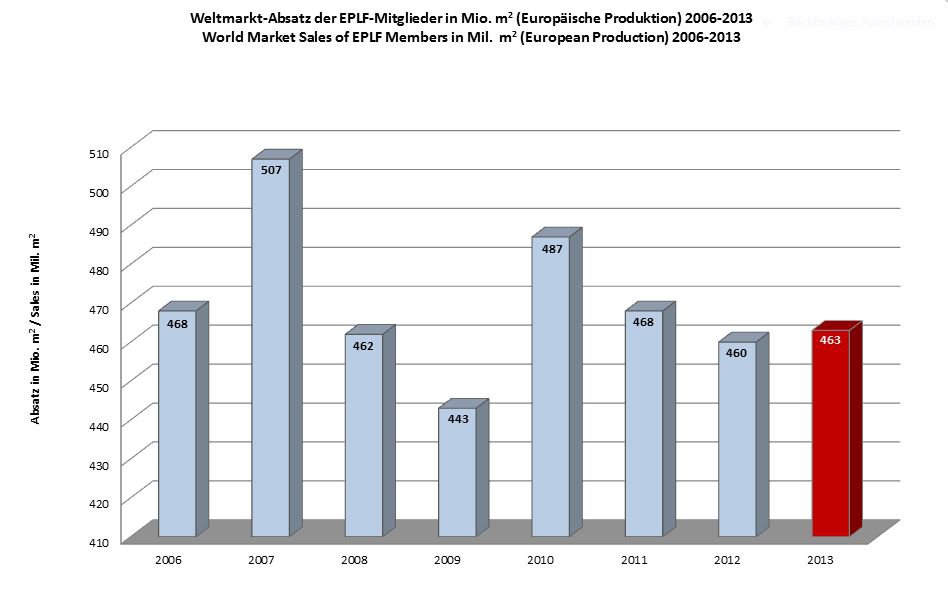

Although the financial crisis does not appear to be completely over yet, the international laminate flooring market is recovering. Growth has been seen particularly in Eastern Europe, as well as in exports to Asia and North America. The upward trend for EPLF producers that began to emerge in the previous year has stabilised. Even though slight sales declines continued to be observed in Western Europe, 2013 remained a good year for the EPLF (Association of European Producers of Laminate Flooring) thanks to gains in the other regional markets.

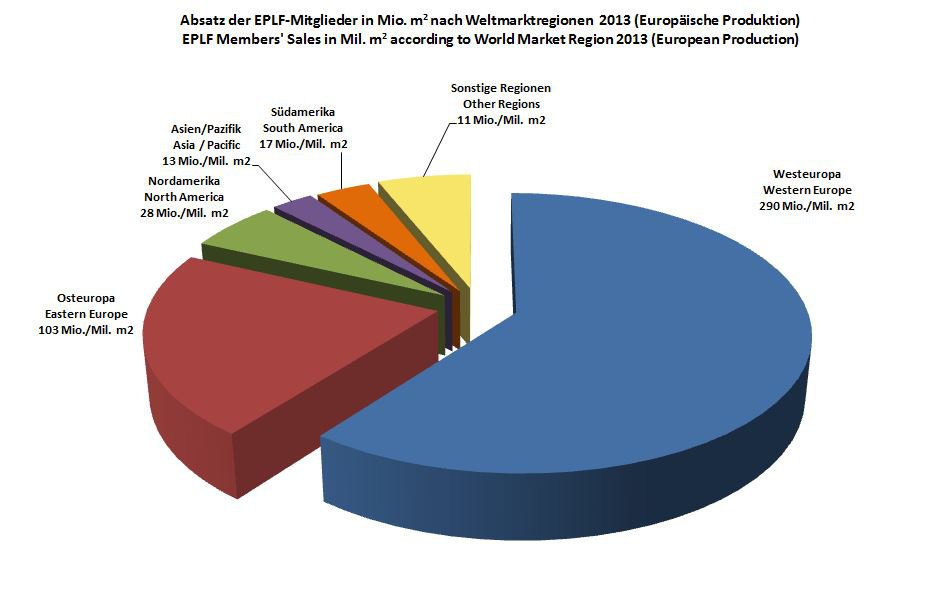

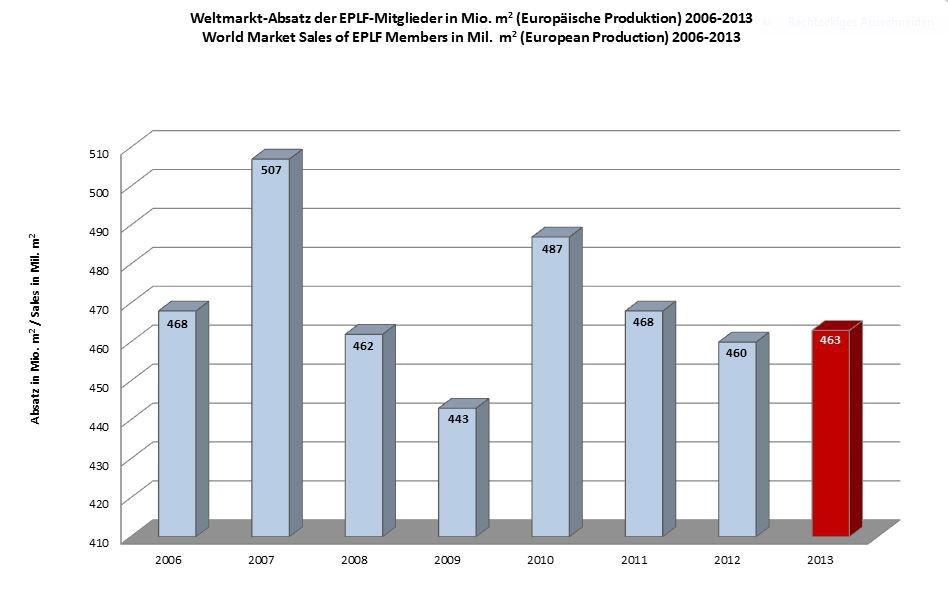

In 2013, the EPLF’s 21 ordinary member companies (manufacturers of laminate flooring) sold 463m m² of European-produced laminate around the globe (previous year: 460m m²), representing a global market sales increase of approx. 0.7%.

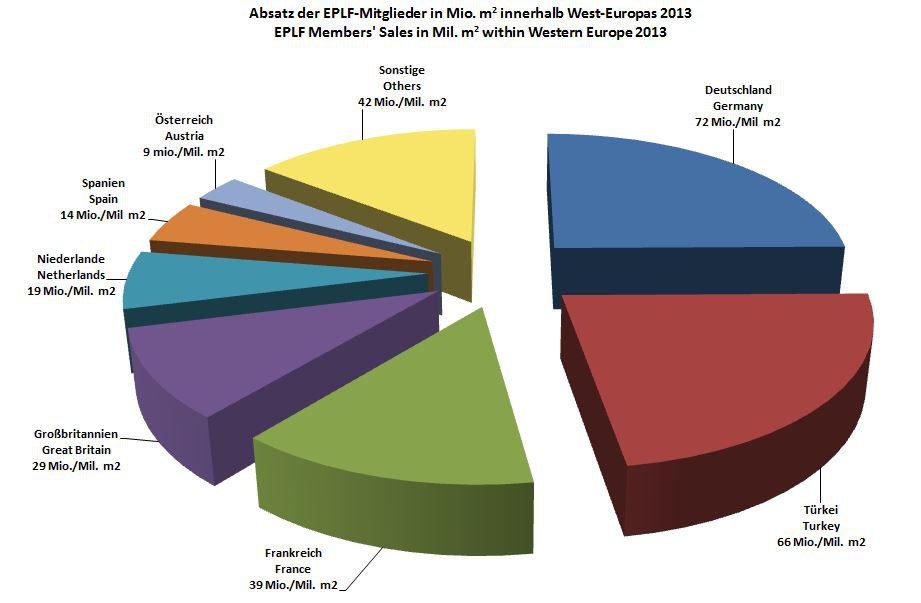

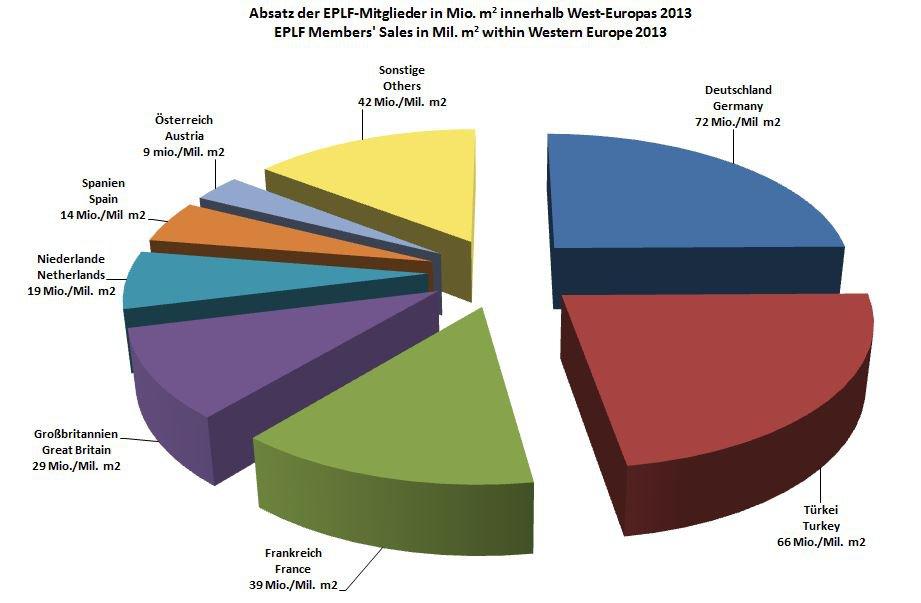

In 2013, the western European core markets in the European laminate flooring industry experienced a slight decline of just under 3% overall. In absolute figures, western European sales fell from 298m m² in 2012 to 290m m² in 2013.

Germany saw a decline with approx. 72m m² (previous year: 76m m²), yet remained the largest single market, leading the ranking of western European markets. Turkey occupied second place with over 65m m² (previous year: 66m m²). This slightly lower but still satisfactory result was achieved partly thanks to the Turkish member companies of the EPLF, and partly due to economic growth in this country. France saw a slight decline with 39m m² (previous year: 40m m²) and continued to hold third place within Europe. The United Kingdom was stable with 29m m² (previous year: 29m m²) and held fourth place, while the Netherlands occupied fifth place with 19m m² (previous year: just under 19m m²). Spain remained in sixth place with 14m m² (previous year: 15m m²).

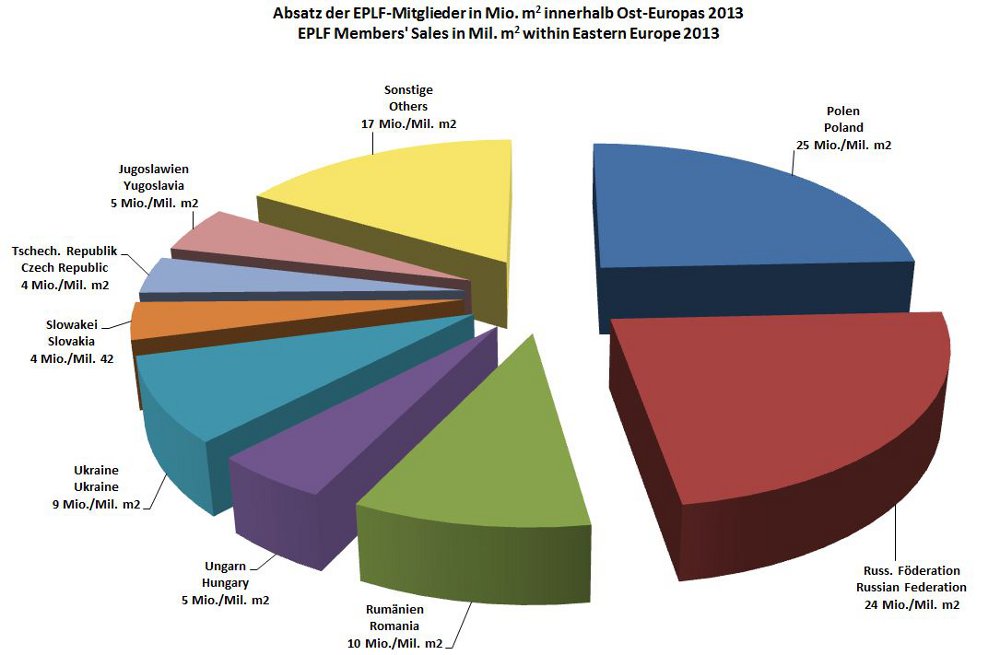

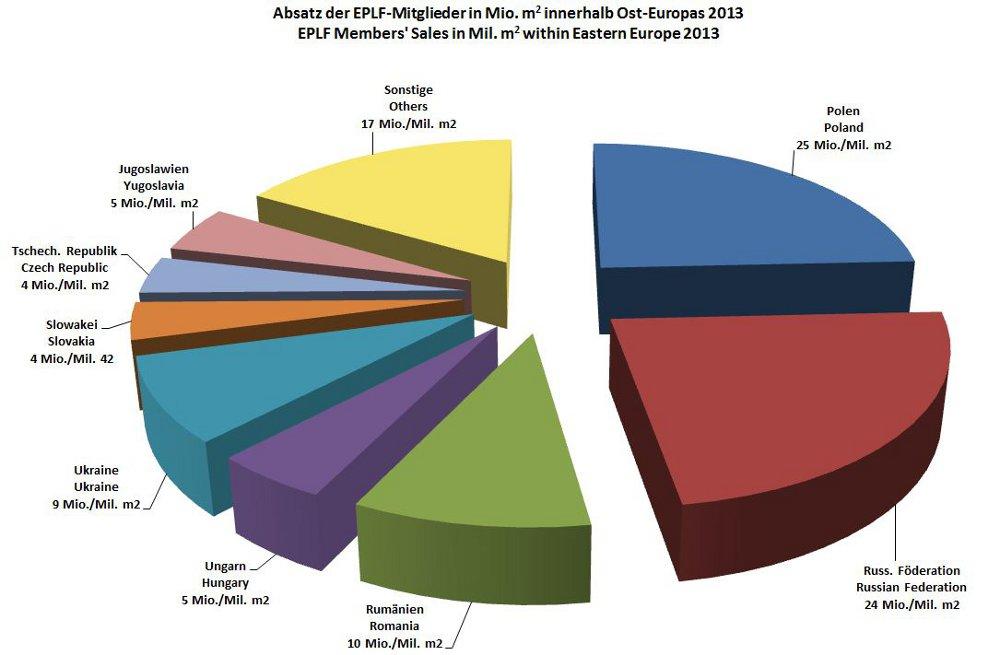

European laminate flooring manufacturers sold 103m m² (previous year: 99m m²) in Eastern Europe in 2013, an increase of 4% compared with the previous year. Poland once again came top with approx. 25m m² (previous year: 24m m²). With 23.9m m² (previous year: 23.7m m²), Russia held a strong second place in the sales ranking, and promises further growth rates in the future. Romania occupied third place with 10m m² (previous year: 9.8m m²), while Ukraine maintained its fourth place with a rise to 9 million (previous year: 8m m²). Hungary remained in fifth place with 4.6m m² (previous year: 4.2m m²).

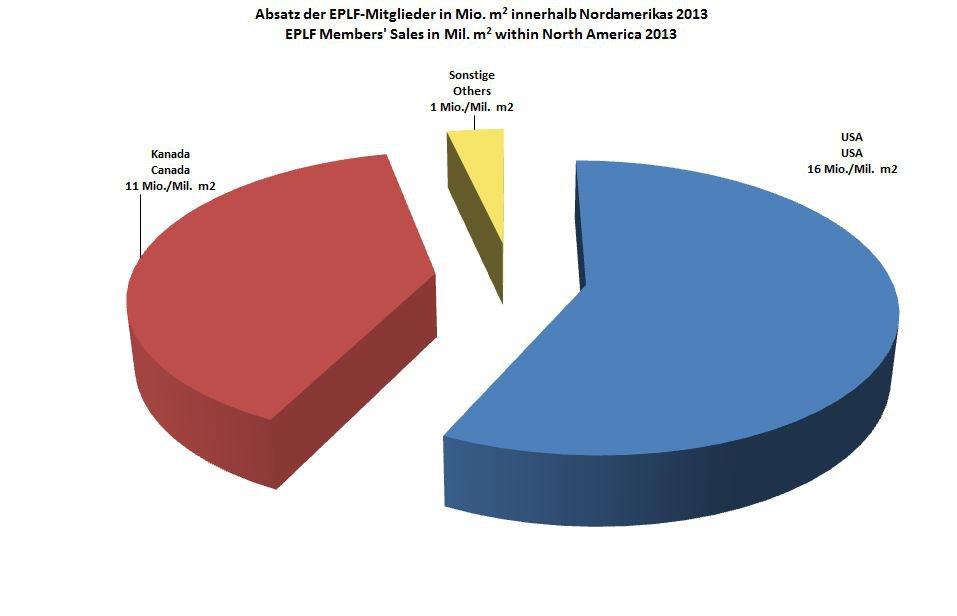

As recently as 2011, North America experienced a dramatic slump: sales dropped from 41m m² in 2010 to 27m m² in 2011, while only 23m m² was achieved in 2012. This was caused by the challenging economic situation in the USA. In 2013, North American sales picked up once more, with 28m m². The USA in particular showed an encouraging result for European laminate flooring manufacturers, with 16m m² (previous year: 12m m²). Canada remained stable in 2013 with 11m m² (previous year: 11m m²).

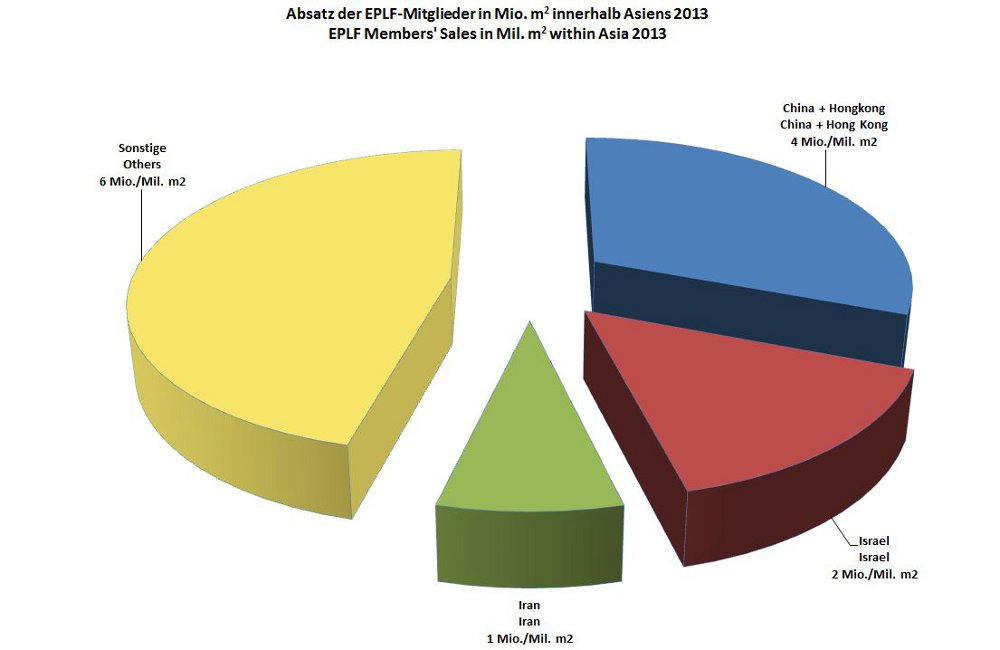

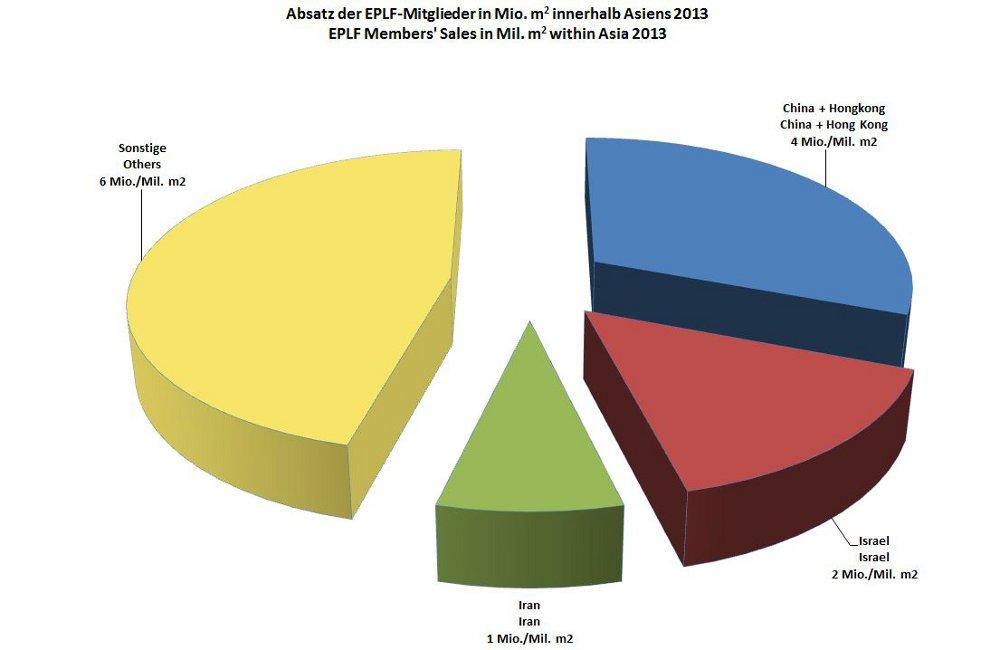

In Asia-Pacific, the total sales of European manufacturers for 2013 stood at approx. 13m m² (previous year: 12m m²), representing a slight increase. The Chinese market, including Hong Kong, showed particularly clear growth due to exports from European producers in the premium sector – this market achieved sales of over 4m m² (previous year: 3m m²) in 2013. The Iranian market fell even further in 2013, achieving less than half of its already rather poor 2012 sales figure of 1.6m m².

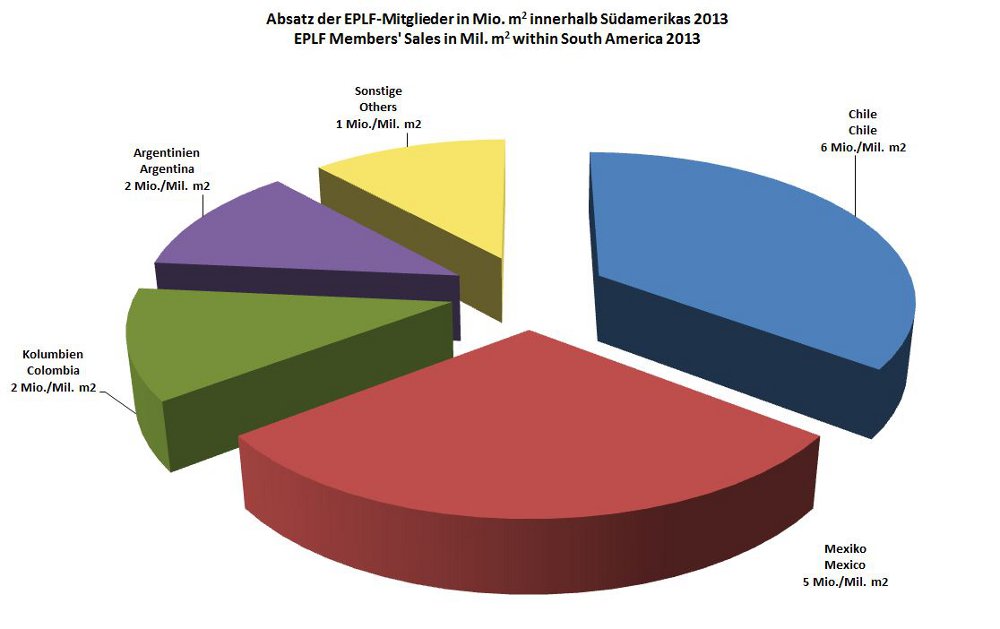

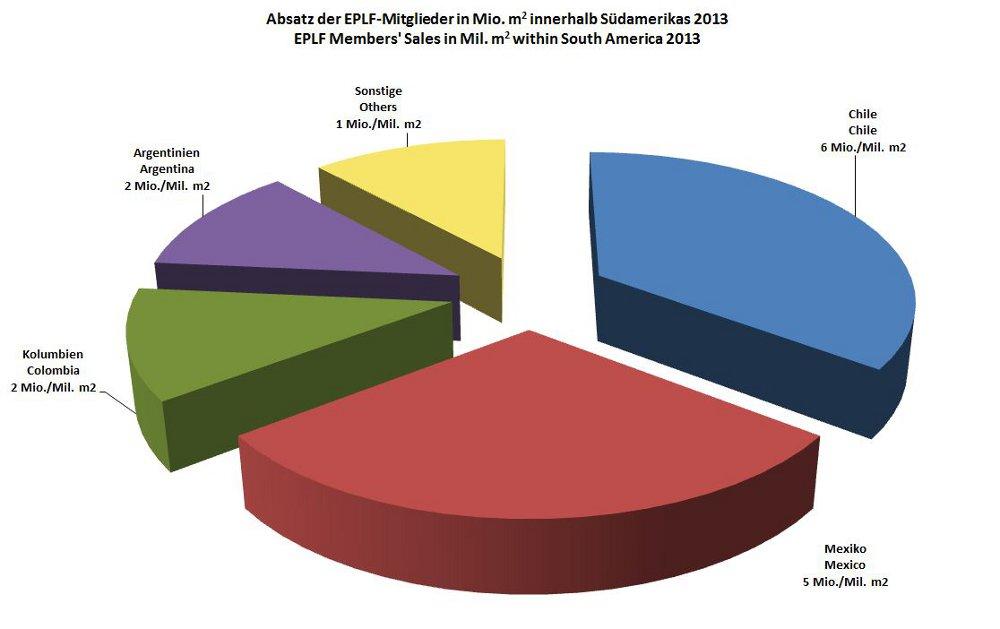

South America remained stable in 2013 with 17m m² (previous year: 17m m²). The Chilean market showed a somewhat disappointing result compared with the previous year, with sales of 6m m² (previous year: 6.5m m²), while sales in Mexico shaped up better, rising to 5m m² (previous year: 4.3m m²).

www.eplf.com and www.mylaminate.eu

Source: EPLF

Have something to say? Share your thoughts with us in the comments below.