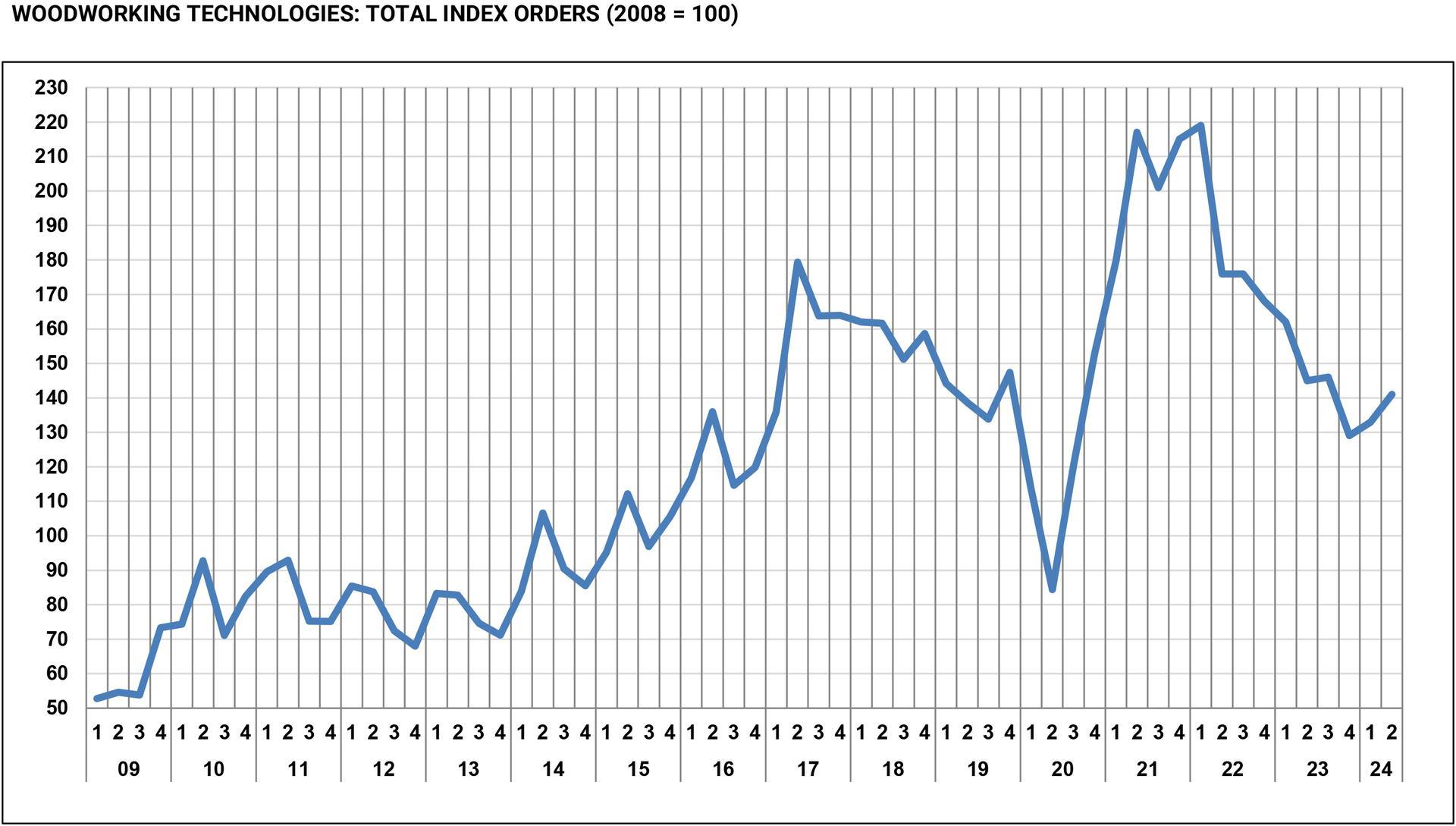

The woodworking and furniture technology business in Italy has seen a reduction in orders over the last nine quarters as the industry adjusts to the two-year post-pandemic boom in which the sector recorded formidable growth. This abrupt return to normal has pushed the indexes back to pre-pandemic levels, and so far, no signs of improvement can be seen.

“We must not surrender to pessimism, as the values are remaining at significant levels,” said Dario Corbetta, director of Acimall, the association of Italian manufacturers. “For sure, the international situation is not supporting companies with an optimistic outlook that would encourage them to reconsider investments in instrumental goods, but the Italian industry remains an excellence of the national offer.”

The quarterly survey by the Studies Office of the Confindustria member association found that from April to June 2024 the industry saw an overall reduction of orders by 2.8 percent compared to the same period of 2023. International orders are unvaried, while domestic orders record a further drop by 5.9 percent compared to twelve months ago.

In addition, the orders book is down to a backlog of 2.9 months, while prices since Jan. 1, 2024, have increased by 0.9 percent.

According to the quality survey, 45 percent of the interviewed companies expect substantial stability in production, while 50 percent predict further reduction and 5 percent an increase. About employment, 80 percent of the respondents – a representative sample of the entire industry – expect a stable trend, while the remaining 20 percent fear a reduction.

Available stocks are stable according to 55 percent of the interviewees, increasing by 20 percent and decreasing by 25 percent.

Such mood is reflected by the results of the forecast survey: as to the domestic market, 50 percent of the sample see substantial stability in the short-medium term, 5 percent expect a growing trend, and 45 percent a reduction. Opinions are quite “aligned” also about the international market: 50 percent believe the trend will remain stable, and things will get worse for 35 percent of the respondents, while 15 percent (so, a 10 percent higher rate of optimistic opinions) are betting on stronger demand from the rest of the world.

Regarding stock levels, 55% of firms report stability, while 20% indicate an increase, and 25% report a decrease. Looking ahead, 50% of respondents expect the domestic market to remain stable, though 45% predict a downturn. Optimism is slightly higher concerning international markets, where 15% of companies expect a positive shift in demand.

Have something to say? Share your thoughts with us in the comments below.