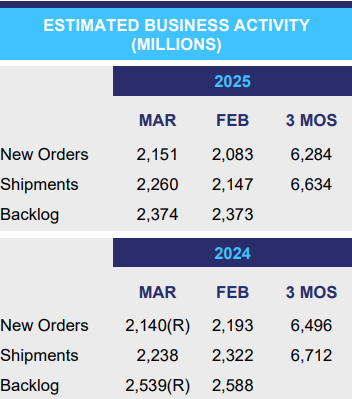

New orders were up 1% in March 2025 compared to March 2024. New orders were also up 1% compared to the prior month of February 2025. However, year-to-date through March 2025, new orders are down 2% compared to 2024.

Shipments were up 1% in March 2025 compared to March 2024, according to Mark Laferriere, assurance partner at Smith Leonard, the accounting and consulting firm that produces the monthly report. Shipments were up 6% compared to the prior month of February 025, which was likely a function of the prior short month (when down 8% to January). Year-to-date through March 2025, shipments remain flat compared to 2024.

March 2025 backlogs were down 6% compared to March 2024 (same as last month), and down 1% from February 2025 as new orders were relatively consistent with shipments during the month.

Receivable levels were down 3% from February 2025, and down 2% from March 2024. Inventories were up 1% from February 2025 and up 3% from March 2024, which are materially in line with prior periods and current operational levels. Inventories and employee/payroll levels are again materially in line with recent months and the prior year.

According to Laferriere and Patrick Willis, Tax Partner, this month's Furniture Insights saw another tariff reprieve as negotiations continue, which hopefully provides some guidance to the industry as to how the situation is going to ultimately play out. Not surprisingly, with this reversal indicating an eventual resolution (or at least short-term stability), consumer confidence rebounded a fter 5 months of declines and respondents indicated an increase in purchasing plans for homes and other big-ticket items.

That is welcome news to the 75% of the Top 100 retailers that posted declines in 2024 as reported recently by Furniture Today. However, the U.S. Census Bureau reported that year-todate sales at furniture and home furnishings stores through April 2025 were approximately 8% higher than the same period of 2024. That 8% is ahead of the relatively flat average orders and shipments reported by the participants in Furniture Insights' monthly stats through March 2025, but hopefully indicates some help is on the way in the form of additional activity, whether driven by looming tariffs or pent-up demand.

Early returns on Memorial Day activity also seem generally positive based upon industry reports. So, with some stock market stability, a slow shift in the housing market, manageable inflation, and a rate cut (or two) later in the year, hopefully the worst of the uncertainty and volatility is behind us and the industry as a whole canadjust accordingly and look forward to a bit of a rebound in the second half of the year.

Have something to say? Share your thoughts with us in the comments below.