BOTHELL, WA -- The Wood Resource Quarterly report of the Global Forest Industry for the First Quarter 2013 is excerpted here.

Global Timber Markets

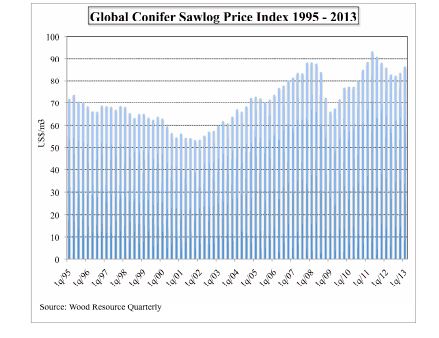

• Sawlog prices were up in practically all regions covered by the WRQ in the 1Q/13, but they were still generally lower than they were in the 1Q/12. The biggest increases from the previous quarter occurred in Western US, Latvia, Finland and Sweden. The Global Sawlog Price Index (GSPI) was up 2.4 percent to US $86.33/m3 from the 4Q/12, the biggest quarter-to-quarter increase since early 2011.

Global Pulpwood Prices

• Wood fiber prices were generally down in North America and up in the rest of the world during the 1Q/13. The Softwood Wood Fiber Price Index (SFPI) in the 1Q/13 was practically unchanged at $99.90/odmt from the 4Q/12. The SFPI has inched downward for seven consecutive quarters and is currently down 8.8 percent from the most recent peak in 2Q/11. The biggest changes in US dollar terms in the 1Q/13 were the declines in chip prices in Eastern Canada (-12.4%), Japan (-8.6%), Western Canada (-7.8%) and the US Northwest (-4.2%). The biggest increases came in France (+10%) and Germany (+6.9%).

• Hardwood fiber prices were down in Asia and Eastern Canada in the 1Q, while they were slightly higher in Europe and Latin America as compared to the 4Q/12.

The Hardwood Wood Fiber Price Index (HFPI) fell by 1.1 % to $103.66/odmt in the 1Q/13, which and was 12 percent below the all-time high in the 3Q/11.

Global Pulp Markets

• Global production of market pulp was 2.7 percent higher the first two months of this year than for the same period in 2012.

• Prices for softwood pulp (NBSK) have trended upward for six months and were in April about $845/ton in Europe. Hardwood pulp (BHKP) prices have moved up at about the same rate.

Global Lumber Markets

• Lumber production in the US and Canada improved during 2012 and early 2013, with total output in 2012 being six percent higher than in 2011. During the first two months of 2013, production levels continued to go up by 9.5 percent in the US and 7.2 percent in Canada as compared to the same period in 2012.

• The US lumber price developments during 2012 and into early 2013 have been quite remarkable with the Random Length Lumber Price Index increasing by almost 85 percent from late 2011 to April 2013.

• Sawmills in British Columbia have become the largest suppliers of lumber to China in recent years, surpassing Russia in 2010. The value of Canadian shipments was about 1.1 billion dollars in both 2011 and 2012.

• Lumber imports to China fell 12 percent to 3.3 million m3 from the 4Q/12 to 1Q/13. This was still seven percent higher than in the 1Q/12. Canada and Russia continue to be the major suppliers, accounting for 78 percent of the total imports.

• Consumption of softwood lumber in Japan has been higher this year than in 2012 and the rise in demand has been met both by higher domestic lumber shipments (+6%) and by an increase in importation.

• Sawmills in both the Nordic countries have expanded shipments to nonEuropean countries during the first quarter. Export volumes to Japan were up 8 and 11 percent for Sweden and Finland, respectively.

Global Biomass Markets

• The wood pellet export industry in North America has grown exponentially in a relatively short period of time. The export value has increased from an estimated 40 million dollars in 2004 to almost 400 million dollars in 2012.

• Pellet prices were close to, or at, record-high levels in all the major markets in Europe in the 1Q/13.

Global timber market reporting is included in the 52-page quarterly publication Wood Resource Quarterly. The report, established in 1988 and with subscribers in over 30 countries, tracks sawlog, pulpwood, lumber and pellet prices, and market developments in most key regions around the world. To subscribe to the WRQ, please go to WoodPrices.com

Source: Wood Resources Intl. LLC

Have something to say? Share your thoughts with us in the comments below.